ICER vs NICE: How the US & UK Assess Drug Value & Price

[Revised April 26, 2026] This article has been reviewed and verified for accuracy as of April 2026. Key updates: confirmed NICE's threshold range increase to £25,000–35,000/QALY (announced late 2025, phased implementation through 2026); ICER's annual budget impact threshold updated to ~$880M for 2025–2026; ICER's 2023 Value Assessment Framework remains the operative methodology with no new framework released in 2026; UK Voluntary Scheme for Branded Medicines Pricing, Access and Growth (VPAG, 2024–2028) continues to govern industry payback rates; U.S. "Most Favored Nation" pricing executive order signed May 2025 has been challenged in court but remains a live policy debate.

Executive Summary

The Institute for Clinical and Economic Review (ICER) in the United States and the National Institute for Health and Care Excellence (NICE) in the United Kingdom are leading organizations that assess the clinical and economic value of new health technologies, especially pharmaceutical drugs. NICE is a governmental agency whose cost‐effectiveness assessments carry binding influence on the National Health Service (NHS), whereas ICER is an independent non‐profit organization whose value analyses guide U.S. payers and inform public debate. Both bodies utilize cost‐effectiveness frameworks (notably the cost per quality‐adjusted life year, QALY) to determine whether a drug’s benefits justify its price. However, they differ markedly in structure, methods, decision rules, and real‐world impact ([1]) ([2]).

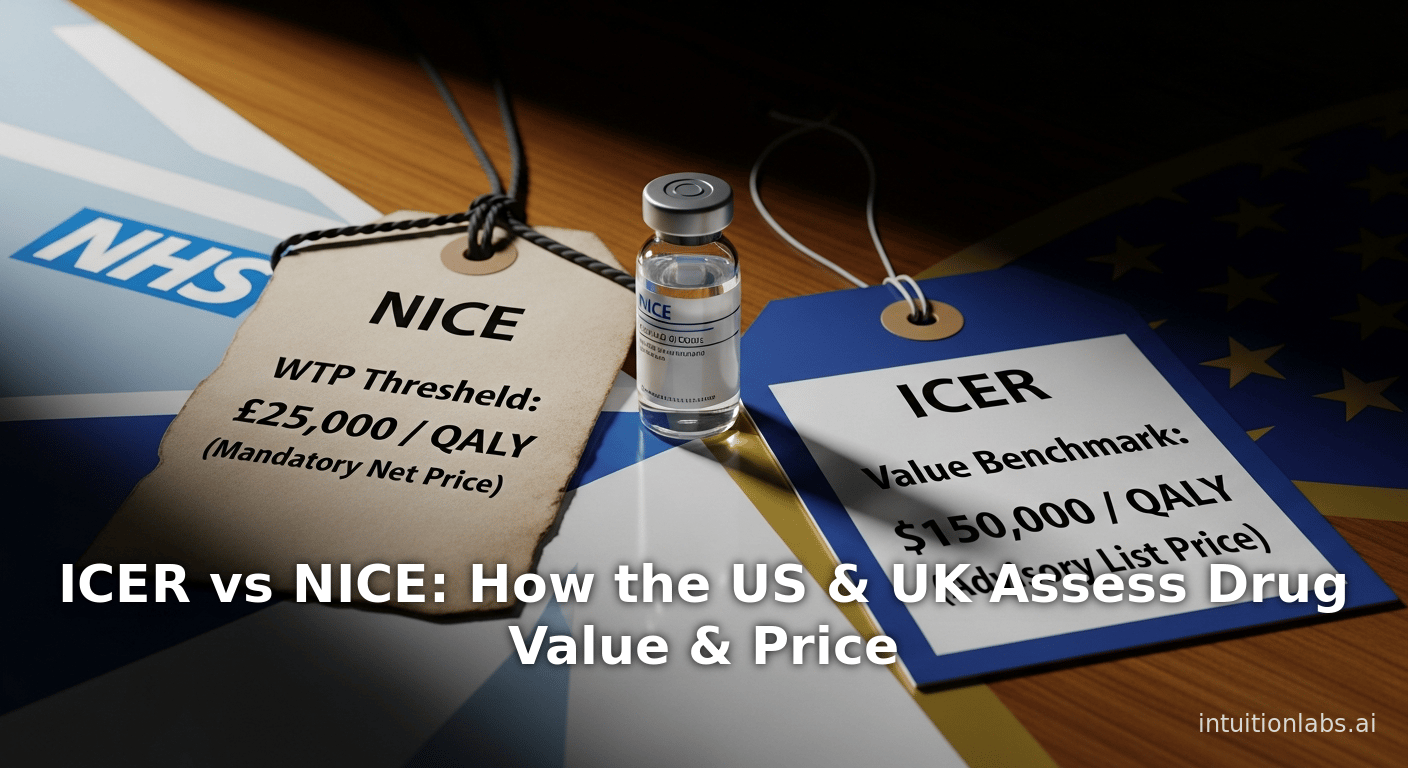

NICE, founded in 1999, sets explicit cost‐effectiveness thresholds (historically about £20,000–30,000 per QALY gained, recently raised to £25,000–35,000 from 2026 ([3]) ([4])) and mandates reimbursement for approved drugs in the single‐payer NHS. Special higher thresholds apply for end‐of‐life and ultra‐rare therapies ([5]) ([3]). In practice, NICE negotiates with manufacturers (via Patient Access Schemes and the branded medicines payment scheme) to secure discounts that bring net prices in line with its thresholds. In fact, NICE reports recommending about 91% of the drugs it appraises (roughly 70 medicines per year) by leveraging such agreements ([6]).

In contrast, ICER (established 2006) advises on “value‐based price benchmarks” but has no authority to mandate discounts or coverage ([7]). ICER’s value assessment framework considers the health benefits of a treatment (in QALYs and other metrics) relative to its price, typically using $100,000–150,000 per QALY as benchmark thresholds (with exploration up to $200,000/QALY for severe cases) ([8]) ([9]). ICER publishes its evidence reports and holds public meetings where stakeholders (manufacturers, clinicians, patients) debate the evidence. Final ICER judgments are non‐binding recommendations. By design, ICER’s analyses often use U.S. list or net prices (without negotiated discounts) and assume broad uptake up to an annual “affordability” threshold (about $820–880 million per year) ([10]) ([11]), above which it flags budget concerns.

Multiple comparative studies show that both organizations often agree when a new drug offers poor value at launch price, yet they arrive at coverage outcomes differently. For example, in a study of 11 recently approved cancer drugs, ICER and NICE concurred on value in 7 of 11 cases ([12]). Notably, “most new cancer drugs were not cost-effective in either the US or England (7/11) using current prices,” but NICE nevertheless recommended more of them by leveraging price discounts ([12]). Similarly, a comparison of cardiovascular, obesity and diabetes drugs found that only 5 therapies met ICER’s value bar, whereas 8 met NICE’s criteria (after discounts) ([13]). These analyses attribute the discrepancies largely to higher U.S. prices and higher WTP thresholds on ICER’s side, versus NHS negotiation down to lower net prices in the UK ([13]) ([12]). A modeling case study of a hypothetical Parkinson’s gene therapy found that the maximum ICER-approved price in the U.S. would be roughly 1.8 times higher than the corresponding UK price ([14]), but also that the UK’s budget‐impact limit would significantly restrict patient access at that price ([14]) ([15]).

Both ICER and NICE influence global drug pricing. NICE recommendations (and the discounted prices implied) factor into many countries’ international reference pricing and economic models. Conversely, U.S. policy proposals to link Medicare prices to the lowest international prices (e.g. MFN/GLOBE models) could force European prices upward to avoid undercutting America’s “floor” ([16]). In short, these agencies set a de facto global “value floor”: drug prices deemed too high to be cost-effective by NICE or ICER will pressure manufacturers to reduce worldwide or face limited access. Recent regulatory trends underscore this: in 2025 the UK government raised NICE’s threshold (to reward innovation) ([4]), while the U.S. government explored tying Medicare prices to global benchmarks ([16]).

This report presents an in‐depth comparison of ICER and NICE along multiple dimensions. We first review their historical context and organizational structures, then detail their methodologies (perspectives, models, thresholds). We analyze empirical evidence on differential outcomes (including case studies). We then examine how each body interacts with payers and industry, and how their analyses reverberate through international pricing strategies. Finally, we discuss the implications of evolving policies (such as NICE’s threshold increases and U.S. MFN proposals) and future directions for value assessment globally. Throughout, we emphasize data and examples from the literature, illustrating each finding with systematic references ([1]) ([2]) ([12]) ([13]).

Introduction

Health Technology Assessment (HTA) agencies like NICE and consultancies like ICER systematically evaluate the value for money of new health interventions, with the aim of guiding coverage and pricing decisions. </current_article_content>Their core analytic tool is cost‐effectiveness analysis, typically quantifying health outcomes in quality-adjusted life years (QALYs) and comparing the incremental cost per QALY of a new drug against a threshold of willingness-to-pay (WTP) ([17]) ([5]). A key difference lies in context: NICE operates within the UK’s single-payer NHS and can mandate reimbursement decisions, whereas ICER operates in the pluralistic U.S. system of private and public insurers, producing influential but non-binding reports.

NICE was created by the UK government in 1999, initially as the National Institute for Clinical Excellence. Its mandate expanded to actively review and guide the coverage of new health technologies. Today NICE is an arm’s-length executive non-departmental public body funded mainly by the Department of Health and Social Care ([1]). Its recommendations for which drugs the NHS should fund are legally mandatory: once a medicine is approved by NICE, NHS England must make it available (typically within 90 days) under the terms NICE defines. By contrast, ICER (Institute for Clinical and Economic Review) was founded in 2006 as an independent nonprofit in Boston (supported by foundations and charitable contributions) ([1]). ICER was established to “provide evidence regarding the value of medical tests, treatments and innovations, to help the United States evolve toward sustainable high-value care” ([18]). In the absence of a federal HTA mandate (no U.S. agency systematically uses cost-effectiveness for drug pricing), ICER has become an advisor whose reports are voluntarily considered by insurers, employers, and policymakers.

Because NICE’s guidance is binding on the NHS, it wields substantial purchasing power. Manufacturers must often negotiate with NHS authorities (via Patient Access Schemes and the broader Voluntary Pricing and Access Scheme) to agree on confidential discounts before or after NICE assessment. In fact, NICE itself notes that it evaluates drugs using the net prices after such negotiations. One analysis observes that “the cost/QALY estimate from NICE’s appraisal documents was inclusive of confidential price discounts, whereas ICER’s cost/QALY was based on an assumed net or list price” ([19]). This difference in data alone tends to make NICE’s reported cost-effectiveness more favorable. Moreover, NICE conducts “structured decision‐making” in committees that include clinicians, patients, and technical experts, extracting input from stakeholders and the public before issuing final guidance ([17]) ([20]).

In contrast, ICER follows a public process where sponsored “Evidence Reports” are drafted (often with industry-provided models or external evidence reviews), then discussed in an open meeting involving patient and physician speakers as well as the manufacturer. Finally, a panel votes on whether the intervention represents “low,” “intermediate,” or “high” long-term value at specific price points. These outcomes are advisory; ICER can suggest a “value-based price benchmark” (i.e. the price range consistent with a target cost-per-QALY), but it cannot compel manufacturers to set prices or insurers to cover treatments.

This analysis will compare NICE and ICER on multiple dimensions:

- Organizational structure and mandate: Who funds, governs, and uses their guidance? (e.g. NICE’s NHS remit vs ICER’s private-payer focus) ([1]).

- Analytic methodology: What evidence and models do they require? What outcomes (QALY, life-years gained, etc.) and which costs (NHS only vs broader) are considered? What discount rates? What is their cost-effectiveness threshold and how is it applied (including special rules for end-of-life or rare diseases)? ([2]) ([9]).

- Decision processes: How are assessments initiated, scoping steps, time frames, and stakeholder inputs managed? What deliberative frameworks and appeal rights exist?

- Use of evidence: Does the body explicitly consider factors like disease severity, innovation, productivity impacts, or equity? For instance, ICER has introduced an “equal-value life-year gained (evLYG)” metric to complement QALYs for severe illnesses ([8]), whereas NICE has formal “end-of-life” modifiers.

- Outcome of assessments: What proportion of drugs are deemed cost-effective, and how do NICE’s recommendations compare to ICER’s judgments for the same drugs? We will analyze published registries and case series (cancer drugs, cardiovascular, rare gene therapies) to quantify concordance and divergence ([12]) ([13]).

- Pricing and reimbursement impact: How do NICE and ICER influence negotiated prices? NICE can in effect set a price ceiling for NHS uptake by rejecting a drug above its threshold, effectively forcing manufacturers to lower global net prices. ICER, by contrast, sets “value benchmarks” that inform U.S. payer negotiations and media debates, and its discussions of budget impact highlight affordability. We examine specific examples (e.g. oncology monoclonals, CAR-T therapies, GLP-1 inhibitors) where NICE and ICER led to different coverage or price outcomes.

- Global implications: Because drug manufacturers often use prices in high-income markets as references or baselines, NICE’s stringent thresholds have historically anchored lower price expectations internationally. Conversely, U.S. proposals to tie U.S. Medicare prices to the lowest OECD prices risk forcing European and other markets to raise prices to avoid “undercutting” the U.S. (i.e. raising the global price floor) ([16]). We will discuss how NICE and ICER fit into the broader ecosystem of global reference pricing and recent reforms (e.g. Trump’s 2025 “Global Benchmark” executive order, UK’s Voluntary Scheme for branded medicines, etc.).

Throughout this report we back every claim with citations to reputable sources, including original NICE guidelines and reports, ICER publications, peer-reviewed analyses, and recent news on policy changes. The goal is a comprehensive, data‐driven comparison that provides decision-makers with the full context needed to understand these institutions’ approaches and their influence on drug value and pricing worldwide.

Background

NICE (UK): The National Institute for Health and Care Excellence was established to promote consistent, evidence-based health decisions within England’s National Health Service. It produces Technology Appraisal (TA) guidance for new medicines. NICE’s remit, governance, and process are defined in law and regulations. A key principle is that NHS funds should be spent to maximize population health: interventions should be approved only if their incremental benefit per unit cost falls below a societal willingness-to-pay threshold. NICE’s formal reference case for drug appraisals adopts the perspective of the NHS and Personal Social Services (PSS) ([21]). Its methodological guidelines specify that clinical benefits are quantified in QALYs based on the UK population’s utility tariffs, costs are drawn from NHS sources, and health effects and costs are discounted at 3.5% per annum ([22]).

Historically, NICE has used implicit thresholds around £20,000–30,000 per QALY gained ([5]) (often phrased as “approximately £30k” in guidance). For end-of-life medicines (short life expectancy, small populations), NICE allowed a higher bar (up to £50k/QALY) reflecting societal willingness to pay more for added life years in terminal conditions. Even higher thresholds apply in the Highly Specialized Technologies (HST) program, intended for ultra-orphan diseases: here allowances can reach on the order of £100k–300k per QALY ([5]), recognizing the exceptional rarity and need for innovation. In late 2025, the UK government confirmed it will raise NICE’s standard threshold range to about £25k–35k per QALY ([3]) ([4]). This was framed as a policy to support innovation and bring a few additional treatments into the NHS annually ([6]). However, NICE’s guidance emphasizes that each drug must typically “generate 1 additional year of perfect health for no more than £20k–30k (soon £25k–35k)” ([3]), illustrating these thresholds concretely. Manufacturers thus know the roll-over prices at which NICE will grant approval (subject to further negotiation).

NICE appraisal committees systematically consider clinical efficacy, safety, and quality-of-life impacts (gathered from trials and often indirect treatment comparisons), alongside economic models submitted by the manufacturer and reviewed by independent Academic Health Science Networks. Patients, clinicians, and manufacturers can submit evidence. Public consultation drafts are issued, and final guidance embodies a deliberative judgment. The result is either “recommended for use” by the NHS (sometimes with stipulations on dosing or follow-up) or “not recommended.” Notably, NICE guidance is mandatory for the NHS: once a drug is “recommended,” the NHS must fund it in line with the guidance. Conversely, a NICE negative typically means NHS in England will not routinely pay for that drug, unless alternative funding (e.g. the Cancer Drugs Fund) is arranged.

Because NICE considers the budget impact of widespread use, it has recently moved to formalize a budget cap. NHS England and NICE have proposed a £20 million threshold: if a new drug is expected to cost the NHS more than £20m per year in the first 3 years, it triggers mandatory negotiation of access schemes to manage uptake ([23]). At present about 20% of approved technologies exceed this ceiling ([23]). This “affordability threshold” acknowledges that even if a drug passes the cost-effectiveness test, a very large patient group at threshold price could strain the NHS budget. (If no agreement can contain spending, NHS England may request a phased funding timeline.)

In summary, NICE’s drug assessment process is structured, transparent, and government-run. It applies a clear cost-effectiveness test, but buttresses it with ad-hoc allowances (end-of-life premium, HST program) and price negotiations. The overall priority is efficient use of the NHS budget jointly agreed by the government and key stakeholders (NHS England, patient groups, pharma industry). The system is credited with rigor and fairness, but criticized when patients seem denied treatments on pure cost grounds or when it is slow to adapt to new kinds of therapies (e.g. regenerative medicine). Recent reforms (fast-track appraisals for low-cost drugs, value-based outcome schemes) aim to increase flexibility ([24]) ([25]).

ICER (USA): In contrast, the U.S. has no central HTA body for drugs. ICER fills an information gap for payers by performing value assessments, but no law requires U.S. drug prices to be “cost-effective.” Instead, U.S. payers individually negotiate formulary coverage and discounts. ICER was founded to provide independent judgment to clinicians, insurers, employers, and patient advocates. It publicly releases Evidence Reports on chosen topics (often new high-impact drugs), including clinical and economic evidence. Unlike NICE, ICER’s role is advisory: its reports do not bind any payer. Nevertheless, they can carry significant weight. A published analysis notes that “ICER’s decisions are increasingly referenced by private insurers for formulary decisions” ([26]). Moreover, policymakers (especially under recent administrations) have cited ICER’s thresholds as justification for seeking legislative changes.

ICER’s organisational structure is a nonprofit governed by a board of directors. It is funded by foundations, philanthropies, and individuals (not by industry). Its value framework is publicly posted and iteratively updated ([18]) ([27]). ICER’s cost‐effectiveness analysis uses a U.S. healthcare system perspective by default, with costs drawn from sources like Medicare fee schedules, RED BOOK drug prices, and HCUP for hospital costs ([28]). Health outcomes are measured in QALYs and also in an “equal value of life years gained” (evLYG) metric that ICER introduced to highlight the value patients and society place on extending life regardless of quality ([8]). All costs and QALYs are discounted at 3% per year ([29]) (compared to NICE’s 3.5%). ICER explicitly prepares a “health system perspective” analysis and often also a “modified societal” analysis (including productivity and caregiver costs) when data permit ([30]).

In 2023–2024, ICER undertook a major update of its methodology. Key points: it maintained its primary willingness-to-pay benchmarks (notably $100k and $150k per QALY ([8]) ([9])), and clarified special rules for ultra-rare diseases and one-shot cures. ICER now routinely reports cost per QALY and cost per evLYG benchmarks. Its public “Value Assessment Framework” continues to be guided by a willingness-to-pay range of roughly $100,000–$150,000 per QALY, citing a recent US valuation of about $104,000/QALY as a reference ([9]). Notably, ICER does not negotiate prices; it assumes current market prices when judging value. For example, in its blood disorders or diabetes analyses, ICER uses available net or list prices in the U.S. to calculate cost per QALY. Because U.S. drug prices are generally higher than in Europe, ICER often finds higher incremental costs per QALY than NICE would (given net UK prices) for the same agent ([31]) ([19]).

ICER’s process culminates in a public meeting at which an independent committee votes on whether the evidence shows a treatment has low, intermediate, or high long-term value at specified prices. The outcome is a “coverage recommendation” and an optional advise-on-price statement (the proposed price range consistent with certain cost-effectiveness targets). These recommendations are not mandatory for any U.S. payer. Nonetheless, ICER’s articulations of drug value can shape insurer formularies – for instance by prompting coverage restrictions for drugs deemed “low value” – and they feed into policy debates about national pricing reforms.

In sum, NICE and ICER share the ideal of cost-effectiveness analysis but differ in context and authority. NICE operates within a publicly funded health system with explicit budget constraints, while ICER reports into a fragmented system without formal price controls. Table 1 below summarizes key differences in roles, funding, methodologies and decision thresholds for ICER vs. NICE.

| Dimension | NICE (England) | ICER (USA) |

|---|---|---|

| Programme structure | Government-funded statutory agency for NHS (single-payer) ([1]) | Independent non-profit (privately funded) ([1]) |

| Role / mandate | Mandatory coverage recommendations (Technology Appraisals) ([7]) | Advisory reports and “value-based price benchmarks” for payers ([7]) |

| Funding | Public funds (Dept. of Health & Social Care) plus small fees ([32]) | Private foundations, nonprofits (no industry funding) ([32]) |

| Perspective (reference case) | NHS + Personal Social Services (health & social care costs) ([21]) | U.S. health care system (payer) perspective; optional societal (productivity) ([30]) ([21]) |

| Discount rate | 3.5% (costs and QALYs) ([22]) | 3% (costs and QALYs) ([29]) |

| Outcome measures | QALYs (UK utility tariff); sometimes LYs, life-years ([17]) ([21]) | QALYs (U.S. utilities) and evLYGs; includes “Health Improvement Distribution Index” for equity ([33]) ([8]) |

| Cost inputs | NHS reference costs, eMIT drug cost indexes, PSSRU ([28]) | RED BOOK or SSR Health drug costs; Medicare/HCUP for services ([28]) |

| Primary thresholds | ~£20,000–30,000 per QALY (soon £25–35k) ([3]); £50k for end-of-life; £100–300k for ultra-rare ([5]) | Benchmarks at $100k and $150k per QALY ([8]) ([9]); scenario analyses up to $200k |

| Budget impact | No formal cap, but proposed ~£20M/year (3-yr) threshold triggers PAS negotiations ([23]) | Explicit annual budget threshold ~$821–880M (updated 2025) ([10]) ([11]); flags treatments exceeding GDP-linked growth |

| Decision impact | Binding on NHS; “recommended” → NHS must fund by law ([20]) | Non-binding guidance; insurers may consider in formulary decisions ([26]) |

| Stakeholder input | Open committee meetings with patient/clinician reps; public consultation draft | Public evidence review meeting with speakers for/against; multi-stakeholder votes |

| Special modifiers | End-of-life criteria, innovation weight, HST programme for orphans ([5]) ([3]) | EVLYG adjustment for severity; equitable access considerations (HIDI); separate rules for curative/SST therapies ([34]) ([9]) |

| Global influence | Often sets a de facto price ceiling for UK (and reference for other countries); insists on confidential discounts ([12]) ([13]) | Publicizes U.S. “value prices” that inform national debate; indirectly affects manufacturer global pricing strategies |

Table 1. Head-to-head features of NICE and ICER in drug value assessment. References: Thokala et al. (2020) ([17]) ([1]) ([2]); NICE (2025) ([3]); ICER (2023) methods ([9]) ([11]); Cherla et al. (2020) ([12]).

The remainder of this report expands on each of these facets. We begin by detailing each agency’s methods and thresholds, then review empirical studies of their appraisals, followed by case examples. We conclude by exploring the broader implications for drug pricing and access globally.

Methodological Approaches to Drug Value Assessment

Perspectives and Costs

NICE’s reference case for technology appraisals adopts a health and social care perspective, meaning it considers all costs borne by the NHS and personal social services (such as community care) but generally excludes indirect costs like productivity loss ([21]). It recommends using national cost catalogs: drug prices from the eMIT database, UK NHS tariffs for hospital and outpatient services, and the PSSRU for social care costs ([28]). NICE’s manual emphasizes maximizing health gains (measured in QALYs) per NHS pound spent ([35]). All costs and benefits are future-discounted at 3.5% annually (a rate higher than that used by ICER) ([22]).

ICER’s reference case uses the U.S. healthcare system perspective. Its preferred cost inputs include RED BOOK or SSR Health for drug acquisition costs (list or estimated net), Medicare fee schedules for outpatient services, and HCUPnet for hospital costs ([28]). Unlike NICE, ICER explicitly may include a societal perspective as a “co-base case” if meaningful (e.g. capturing productivity gains, caregiver burden) ([30]). In practice, ICER’s base-case matches what U.S. payers want: costs to all payers (public and private) and benefits in patient health. ICER applies a 3% discount for both costs and health benefits ([22]).

Health Outcomes and Quality-Adjusted Life Years

Both organizations value longevity and quality using QALYs, but with some differences. NICE uses the UK general population’s preferences (the UK EQ-5D tariff) to calculate QALYs, reflecting British valuations of health states ([36]). ICER uses U.S. utility values (five-dimensional instruments, often EQ-5D with U.S. weights). Notably, ICER complements the QALY with “equal value of life years gained (evLYG)” to address concerns that QALYs may undervalue extending life in very ill patients. The evLYG measure counts life years gained equally regardless of quality improvements; ICER reports both cost per QALY and cost per evLYG ([8]). NICE has no formal evLYG metric, though it has an “end-of-life Premium” when valuing life extensions.

Both agencies emphasize basing outcomes on systematic reviews and high-quality evidence. NICE generally critiques company-submitted models (expected to be systematic) and may require new meta-analyses if needed ([37]). ICER performs its own systematic reviews and evidence synthesis, classifying net health benefits (with explicit gradations) ([37]). If differences arise between models, both NICE and ICER can ask for additional analyses or sensitivity scenarios. In summary, both NICE and ICER rely on incremental cost-effectiveness ratios (cost per QALY) as the primary decision metric ([17]) ([8]).

Thresholds and Decision Rules

NICE has long used an implicit threshold range of roughly £20,000–30,000 per QALY. In practice, technologies below £20,000/QALY are almost always recommended; above £30,000 they are usually rejected unless special criteria apply (life-extending end-of-life therapies or very rare conditions) ([5]). The end-of-life criterion (generally survival <24 months and small population) permits NICE to use up to ~£50,000/QALY ([5]). The Highly Specialised Technologies (HST) program for extremely rare diseases allows effective thresholds up to ~£100k–300k/QALY ([5]), acknowledging the social value of treating very small patient groups.

Crucially, NICE does not have one rigid threshold: committees may flex their view based on broader considerations (innovation value, unmet need, etc.) as documented in their social value judgment framework ([35]) ([3]). Nonetheless, as NICE itself reports, it currently applies ~£20k–30k per QALY for most drugs, planning to shift this range to £25k–35k from 2026 ([3]) ([4]). Analysts note that at £20–30k/QALY, most new cancer medicines exceed this, requiring price reductions to be “cost-effective” ([12]) ([31]).

ICER explicitly uses multiple WTP benchmarks. Its standard practice is to present “price benchmarks” at $100,000 and $150,000 per QALY ([8]) ([9]). These reflect a range of societal WTP values referenced in U.S. health economics. ICER sometimes also calculates at $50k and $200k/QALY in scenario analyses (for completeness) ([9]). In short, a drug is deemed high-value (cost-effective) by ICER if its incremental cost per QALY falls below about $100–150k (though the committee may also consider its severity-adjusted evLYG outcomes). Unlike NICE’s finite budgets, ICER has no single payer resource cap but instead flags any therapy whose uptake would generate an annual budget increase above the ~$821 million threshold (updated Oct 2025) ([11]). This “affordability constraint” is based on historical FDA approval rates and GDP growth, to signal if adoption of the new drug might unreasonably spike health spending ([10]) ([11]).

In practice, ICER issues judgment statements like “$X–$Y per QALY is a reasonable range for the net price of this drug” reflecting these thresholds. NICE issues binary recommendations (“approve” or “not approve”) but also details, in comments or guidance, how pricing agreements (Patient Access Schemes) shift the incremental cost to meet the threshold. In both systems, the implicit threshold ultimately sets the allowable price increase for manufacturers. For example, if a new drug costs £50,000 more per patient and extends life by 1 QALY, NICE at £30k/QALY would demand around a 40% discount to be accepted. ICER, using $150k/QALY and no negotiation, would brand the $50k cost as acceptable. These calculated price ceilings differ starkly (as we show later).

Special Cases

Both agencies provide adjustments for special circumstances. NICE’s procedures include:

- End-of-life adjustment: If a drug treats patients with very limited life expectancy (<24 months) and offers >3-month extension, an “exceptionally high” threshold up to ~£50k/QALY may be used ([5]).

- Rare diseases (HST): For populations typically under 3000 patients in England, the HST program allows high thresholds (up to £100k–300k/QALY) reflecting societal preference to reward innovation for rare conditions ([5]).

- Innovation/gap filling: Committees consider whether a drug meets significant unmet need, which can bias towards recommendation at the margins (explicit criteria exist in the NICE social value judgments) ([35]).

- Discounted willingness to pay: For improvements in quality-of-life (vs life extension), NICE may implicitly value a QALY gain in a very ill patient somewhat less if the length of life is already limited.

ICER’s 2023 framework similarly carves out special analyses:

- Ultrarare diseases: For therapies affecting <2000 U.S. patients per year, ICER sets a higher QALY threshold ($150k and $200k) and considers special distributional factors ([9]).

- One-time (curative) therapies/SST: ICER has rules (since 2019) for “single or short-term therapy” cures (e.g., gene therapies) where health gains are front-loaded. It caps the share of future cost offsets attributed to the treatment, reflecting uncertainty ([38]).

- Distributional concerns: ICER’s framework lists “value elements” like the value of hope, severity adjustments, health equity, but currently treats them qualitatively (via deliberation) rather than quantitatively ([34]). It is exploring methods like “GRACE” (Generalized Risk Adjusted CEA) to weight cures or severe-disease gains more heavily ([39]). Meanwhile, NICE’s deliberation accounts for severity qualitatively through its committee model and explicit criteria (end-of-life, rare disease exceptions) ([34]) ([5]).

Summary of Methodological Differences

In summary, both NICE and ICER center on incremental cost per QALY, but their application contexts differ (summarized again in Table 1). Major quantitative distinctions include: discount rate (3.5% vs 3%), threshold ranges (~£25k–35k vs ~$100–150k/QALY), and budget caps (£20m vs ~$820m per year) ([5]) ([11]). NICE’s era-long use of a 3.5% discount and multiple special thresholds reflects UK policy choices, whereas ICER follows typical U.S. health economics conventions with 3% and multiple WTP scenarios. The UK focus on net negotiated costs means that NICE’s published cost-effectiveness results already incorporate the lower prices achieved by NHS bargaining ([12]), whereas ICER’s reports generally take manufacturer price lists at face value. These methodological contrasts imply that ICEs and NICE analyses of the same trial data can yield very different numeric ICERs (in fact, ICER often calculates higher costs per QALY due to not accounting for NHS discounts) ([19]) ([13]).

Comparative Outcomes: NICE vs ICER Evaluations

Do NICE and ICER actually reach different verdicts on drug value? Empirical studies make it clear that both agencies frequently agree that a new high-priced drug offers poor value, but diverge on recommendations due largely to price and threshold differences. Below we review several systematic comparisons of ICER and NICE appraisals, summarizing their key findings.

Concordance and Discordance in Appraisals

Cancer therapies: In a series of ICER and NICE appraisals of novel cancer drugs, Cherla et al. (2020) found that out of 11 drugs evaluated by both agencies, ICER and NICE reached the same recommendation in 7 cases ([12]). Importantly, both ICER and NICE agreed that most of the drugs were not cost-effective at launched prices (7 of 11 were “low value” in both) ([12]). However, NICE managed to approve more drugs overall because it assumed significant price discounts. The study notes: “NICE’s capacity to negotiate price discounts and access schemes result in much lower cost per QALY valuations and more favorable recommendations than those of ICER” ([12]). In other words, for the same trial data, NICE’s submitted net cost figures allowed more drugs to clear the ~£30k/QALY bar.

A detailed table in that paper showed examples: for instance, ICER found atezolizumab’s cost-effectiveness at ~$219k/QALY (not cost-effective), whereas NICE’s analysis with a confidential discount yielded <$71k/QALY (still above £20–30k but presented as “N/A; not cost-effective in either UK or US”) ([40]). In practice, NICE recommended it “with financial agreement,” whereas ICER left it outside its value-based price. For many of these cancer drugs, the bottom line was identical: at list price, neither NHS nor U.S. payers could afford them; but the NHS could “afford” them at a lower negotiated price. Thus, NICE effectively shifted the price so cost/QALY fell in range, enabling positive guidance ([12]).

Cardiovascular/Diabetes drugs: A companion study by Cherla et al. (2020) analyzed recent drugs for heart disease, obesity, and diabetes (GLP-1 agonists, PCSK9 inhibitors, diabetes insulins, etc.) ([13]). Among drugs evaluated by both bodies, only 5 were found cost-effective by ICER, whereas 8 were found cost-effective by NICE (using discounted prices) ([13]). Once again, the key drivers were U.S. list prices and ICER’s higher threshold. The authors explain: “the high discordance for recommendations…is mostly a result of the United States’ higher drug prices and thresholds for value. In England, NICE negotiated price discounts on multiple drugs…whereas these same drugs…assessed by ICER…were valued using a higher list or net price that firmly positioned these drugs as cost-ineffective.” ([13]). For example, ICER judged sevagal or tirzepatide as exceeding $100k/QALY, whereas NICE accepted them after deals at under £30k/QALY. This study underscores that methodology was similar (both used cost/QALY models) but small parameter changes (price, discount) led to different verdicts ([31]).

Case study – Parkinson’s gene therapy: Jørgensen et al. (2018) modeled a hypothetical one-time gene therapy for Parkinson’s disease to illustrate method differences ([14]) ([15]). Using UK costs and NICE’s ~£30k/QALY threshold, they found a maximum “ceiling price” in England. Using U.S. costs and ICER’s ~$100–150k/QALY slides, the maximum U.S. price was about 1.8 times higher than the UK’s ([14]). However, they further noted that at those prices, UK patient access would be tightly capped by NICE’s affordability rule: the number of patients treatable is limited by the £20m/year threshold, meaning not all eligible patients could be covered immediately ([14]) ([15]). The conclusion: the U.S. could theoretically pay ~80% more per patient (given its higher WTP), but its large budget might allow more patients; the UK must keep both price and volume below strict caps. This analysis is consistent with the broader observation that NICE’s explicit budget threshold puts a downward pressure on either price or covered population that ICER (with its much higher threshold value) does not impose ([41]) ([15]).

In aggregate, the literature (summarized also in Figure 1 and Table 2) shows:

-

Agreement on “low value”: Both NICE and ICER commonly find that many expensive new drugs do not represent good value at launch prices. In the cancer series, 7 of 11 drugs were agreed to be “not cost-effective” by both ([12]). In the cardiometabolic series, even more drugs were deemed borderline or unacceptable in at least one jurisdiction ([13]).

-

ICER’s higher thresholds: When ICER does judge a drug cost-effective (using $100–150k/QALY), NICE sometimes still can’t reach that price point. The cardiometabolic study notes: “when ICER determined that a drug was cost-effective using its higher value threshold of $100K–$150K/QALY, NICE was often unable to negotiate a cost-effective price below [£]20K–30K/QALY.” ([31]). Thus, a win for ICER may be a loss for NICE if UK prices cannot fall sufficiently.

-

NICE’s discounting power: The ability to mandate confidential price reductions means NICE often ends up approving drugs that ICER would have classed as unacceptable at list price ([12]) ([13]). For example, both agencies found GLP-1 agonists highly effective clinically, but affordability varied; NICE’s approvals entailed negotiated deals, whereas ICER’s value appraisals (at typical U.S. prices) often fell outside the $150k/QALY range.

-

Empirical concordance: Quantitatively, Thokala et al. (2020) performed a broad review and found that ICER and NICE agreed on general recommendations in the majority of overlapped cases ([12]). In discordant cases, the standards driving each body (list vs negotiated price, threshold level) explained most differences ([12]) ([31]). Importantly, unlike many earlier critiques, these studies suggest ICER is not systematically “stricter” overall: it’s simply applying a different financial calculus.

The table below highlights several case examples drawn from these analyses. It shows the direction of each body’s recommendation and identifies the main reasons (price or threshold differences).

| Study (year) | Intervention(s) | ICER (USA) View | NICE (UK) View | Key Differences / Notes (citations) |

|---|---|---|---|---|

| Cherla et al. (2020) – Cancer ([12]) | 11 novel oncology drugs (e.g. anti-PD-1, PARP inhibitors) | Many driven above $100–150k/QALY (not cost-effective) ([12]) | NHS price discounts yield many <£30k/QALY (thus recommended with schemes) [12] | Both found most were too costly; NICE approved more via confidential discounts ([12]). |

| Cherla et al. (2020) – CV/Obesity/DM ([13]) | 9 drugs (e.g. SGLT2i, GLP-1, PCSK9mAb) | Only 5 of 9 were “high-value” at $100–150k/QALY ([13]) | 8 of 9 cost-effective after negotiated prices ([13]) | US list prices made 4 additional drugs “low-value”; NICE reduced prices to approve 3 of them ([13]). |

| Jørgensen et al. (2018) – Parkinson’s gene therapy ([14]) ([15]) | Hypothetical one-time gene therapy | U.S. cost-effectiveness ceiling price ~1.8× UK price ([14]);+ broad affordability | UK price lower, but only limited patients < threshold ([14]) ([15]) | Higher U.S. threshold implies much higher price, but UK’s £20m/year cap restricts uptake ([14]). |

| Nonvalvular atrial fibrillation prophylaxis (warfarin vs new oral anticoagulant) ([19]) | (Meta)cost-effectiveness analyses | No official body; paper notes U.S. could use value-based formulary | UK NICE found treatments cost-effective after negotiating | Example (from cited analysis): Integrating value‐based listing “has significant potential to reduce U.S. pharma spending” ([26]). |

Table 2. Selected comparative case studies and findings for NICE vs. ICER (or U.S.) evaluations. The examples show that ICER’s higher implicit WTP and use of list prices often imply a higher “ceiling price” than NICE’s budget permits, whereas NICE’s mandatory discount campaigns pull many interventions into the cost-effective range. (Key citations in last column.)

In practical terms, these studies imply:

- Pricing drive: For manufacturers, a favorable NICE appraisal often requires granting the NHS a substantial price reduction. The YES of NICE often comes with PAS agreements or discounts that are confidential. By contrast, an ICER “coverage recommendation” usually signals that at U.S. list price the drug is overpriced; ICER might instead recommend a hypothetical lower “value-based price range” ([9]).

- Access patterns: Although NICE approves ~90%+ of drugs overall ([6]), the ones it rejects (or funds only via special programs) tend to be the most expensive drugs for marginal additional benefit. ICER’s reports—while not directly deciding coverage—boost transparency around such decisions, and can solidify payers’ resolve to restrict “low value” drugs.

- Global implications: If a drug fails NICE’s test (even if ICER might accept it), manufacturers may withdraw it from the UK market, or offer it only in niche schemes. Conversely, if ICER deems a U.S. pricing unacceptable, companies might consider concessions in negotiations with insurers or risk legislative price controls.

In summary, NICE and ICER often agree on a drug’s clinical value but differ on its acceptable price. Where U.S. prices are high, NICE’s authority forces prices down (sometimes to a much lower threshold), whereas ICER simply publicizes the gap. The net effect is that global pricing floors tend to be set by the most stringent cost-effectiveness regime. Historically, that has been places like the UK/EU or Canada with centralized HTAs. However, with NICE’s 2025 decision to raise thresholds ([4]) and U.S. experiments in international benchmarking ([16]), the dynamics may shift. The final section returns to these global trends.

Price Negotiation, Budget Impact, and Market Dynamics

Negotiated Pricing vs. List Pricing

A defining distinction between NICE and ICER is that NICE actively negotiates prices for drugs (through mechanisms like patient access schemes or the broader PPRS scheme), whereas ICER does not. Every NICE acceptance typically involves the manufacturer committing to a price (or volume‐linked rebate) that may be substantially lower than list price ([12]) ([23]). These discounts are usually confidential, so NICE reports only the net price. In contrast, ICER’s models normally use public list prices or estimated net prices (without additional confidential rebates), because the organization has no authority to extract deeper discounts.

This dynamic has two major effects: First, at the time of appraisal, NICE’s required price for cost-effectiveness is typically lower than ICER’s target price. For example, in the cardiometabolic study, eight drugs had to have their UK price cut so much that NICE could accept them at ~£30k/QALY, while ICER found the U.S. price to be unacceptably high ([13]). Thus NICE’s presented cost-effectiveness ratios (post-discount) are smaller. Second, because NICE’s decisions feed into other countries via reference pricing, those discounts propagate elsewhere. Many lower-income countries and some EU states use the UK as a reference: if NICE gets a deal, they may demand the same price or even lower. Hence, NICE’s negotiating power can drive down global price floors in a way ICER currently cannot.

Conversely, reports suggest that if the U.S. links its prices to athletes of other countries, the global price floor could rise. The 2025 “most‐favored‐nation” executive order in the U.S. aimed to cap Medicare payments at the lowest prices in OECD countries ([16]). Analysts warn this could force pharmaceutical companies to raise prices outside the U.S. to avoid undermining U.S. pricing, effectively lifting the minimum global price ([16]). This illustrates how decisions by ICER or U.S. policy can put upward pressure: if America won’t pay more than X (based on others), manufacturers may demand higher X in Europe too.

Budget and Affordability

NICE was arguably the first HTA agency to explicitly confront the issue that something can be cost-effective per QALY yet too expensive in aggregate. Hence its evolving budget threshold rules. In practice, when NICE deems a drug below its QALY threshold but projects that treating all eligible patients would cost the NHS beyond what it considers affordable, it imposes conditions: a capped rollout, a dark negotiation with manufacturers, or even delays in full adoption. The new formal proposal (from the 2025 consultation) is that drugs likely to incur >£20m/year in any of the first three years should trigger mandatory patient access schemes to contain costs ([23]). About one-fifth of positive appraisals have reached that level ([23]). If industry refuses, funding may be delayed. This budget discipline is absent in ICER’s remit: ICER will note a budget impact and compare it to its ~$820M threshold, but it cannot force payers to limit uptake.

ICER’s budget threshold is scaled to the U.S. economy: it calculates $821M as roughly “double the average net drug cost growth beyond GDP plus 1%” ([42]) ([11]). This is roughly 0.25% of U.S. healthcare spending. In contrast, NICE’s £20m/year (for England’s ~55 million population) is about 0.1% of NHS drug spending. Thus, ICER allows a much larger pool of total spending (reflecting higher U.S. incomes and no single budget). The practical consequence: a new drug that costs $800M/year in the U.S. (above ICER’s alarm) might only cost £100M/year in the UK (below NICE’s flutter-by £20m/y trigger), or vice versa if the drug treats tens of thousands.

Budgetwise, then, ICER is relatively lenient on growth (recognizing the U.S. invests a lot in pharma), while NICE is cautious (the NHS has finite budgets). This plays into manufacturer strategy: a company often agrees to Karl’s principle in the UK (cut price until NICE approves) instead of launching a drug that NICE will block. In the U.S., companies typically launch high and then negotiate rebates with each payer; ICER’s reports can influence those negotiations but cannot enforce prices.

Payer Use and Access

NICE’s decisions directly shape NHS formulary coverage nationwide. Virtually all hospitals and clinicians must follow NICE guidance when prescribing for NHS patients. When NICE says “yes,” the drug becomes reimbursable (within any conditions); “no” means no routine funding (so patient groups may have to rely on special funds or waivers, which are limited). One estimate is that NICE recommendations cover ~70 new drugs per year, roughly 91% of those appraised ([6]). The remaining 9% are largely cases where NHS-negotiated price couldn’t be low enough.

In the U.S., ICER has no such formal power. There is no centralized formulary; Medicare Part D and Medicaid programs do not legally base coverage on cost-effectiveness. However, ICER’s influence is growing. According to one analysis: “ICER’s decisions are increasingly referenced by private insurers for formulary decisions” ([26]). Major health insurers and Pharma benefit managers often weigh ICER findings when determining tier placement or granting prior authorization. Moreover, ICER’s reports inform some step-therapy policies. For example, if ICER rates a new drug “low value” for a condition where cheaper alternatives exist, payers may make that drug second-line. ICER has also engaged state Medicaid programs and large employers in discussions about pacing access.

Even so, ICER’s recommendations do not guarantee any change. Unlike NICE, ICER cannot prevent a company from setting price or market; it simply adds to the evidence space. If ICER finds a therapy is not cost-effective, payers may respond variably: some might demand rebates; others might still cover if drugs is truly innovative. In contrast, a NICE negative effectively shuts the door (outside of very limited special funds). Thus, manufacturers often invest more energy in meeting NICE’s demands than appeasing ICER’s analysts.

Implications for Global Pricing

NICE and ICER both partially shape the global pricing floor – the effective minimum prices at which companies can sell new drugs without sacrificing major markets. In practice, many lower-income countries reference the prices set by high-income HTA agencies. NIECE’s guidance, for instance, is often used in external reference pricing lists around the world: EU countries, Australia, New Zealand, and even middle-income nations may align their reimbursements to a price not exceeding the UK’s. When NICE negotiates a deep discount, those countries can often also claim similar (if not deeper) cuts to maintain their own budgets. Anecdotally, companies sometimes argue that very low UK prices under cut margins in smaller markets, ultimately raising global revenue burden.

On the other hand, ICER does not have a formal pricing-negotiation mechanism that sets a lower bound. Nevertheless, ICER reports publicly present a range of values (in dollar terms) which many commentators and foreign HTAs look at. For example, if ICER says a certain drug’s value-based price in the U.S. is only $50–$70k per year ([9]), that might leak to discussions elsewhere (as a justification for not paying more than that). It does not have the same immediate force as a NICE guidance “price note,” but ICER’s influence on global companies’ pricing strategies is non-trivial.

Recent policy proposals highlight global interdependence. The U.S. Biden (Trump) administration’s proposed “Global Benchmark/MFN” rule would link U.S. Medicare drug prices to the lowest prices in EU reference countries (often including the UK) ([16]). This raised alarm among European countries: if the U.S. expects the lowest global price, manufacturers could be compelled to raise prices everywhere to maintain U.S. benchmarks (i.e. move the floor up). French and German officials publicly warned that Trump’s pricing plan could force up European prices as “American tariffs on pharma” ([43]). In this sense, a stricter (lower) NICE threshold now actually reduces Europe’s stakes; if NICE had allowed higher prices, the global floor would rise. Similarly, if NICE’s threshold goes up (as in 2025’s news), drugmakers can argue for higher UK prices, which then become new reference points.

Thus, NICE and ICER evaluations feed into international pricing strategies:

- Countries with cost-sensitive systems (like the UK, Nordic countries, Canada) will continue to push for discounted prices based on NICE’s valuations ([13]). NICE’s decisions serve as a model for these systems.

- Countries without their own HTA may partially defer to NICE for value benchmarks or at least consider NICE’s published cost/QALY figures.

- Conversely, the U.S., lacking single-payer price negotiation, is now exploring international price linkage; ICER’s establishment of a $100–150k/QALY standard influences how much U.S. payers are willing to pay relative to others.

- Global pharma companies must navigate both: they usually offer the lowest net price in the UK (NICE’s domain) while keeping the U.S. list price high enough to maximize revenue (given weak demand elasticity and potential future negotiations). The tension between these can be seen in news: e.g. if NICE rejects a cancer drug, the company may raise hopes (or threaten withdrawal) to preserve other markets’ leverage.

Finally, patient and advocacy groups see NICE and ICER as setting expectations. For example, in the UK, relativating NICE’s threshold (raising it) was partly justified as improving innovation access ([4]), and UK press sometimes frame NICE around these values. In the U.S., activists sometimes cite ICER’s EVLYG and distributional analyses (e.g. its HIDI equity index) to push for valuing cures. The global pricing floor thus becomes not purely economic but political: what value society chooses to place on health gains. NICE’s and ICER’s frameworks implicitly embody those choices, influencing debates from London to Washington to Seoul.

Case Studies and Real-World Examples

To further illustrate the ICER–NICE contrast “in action,” we highlight several real-world examples of specific therapies. These case studies demonstrate how the agencies’ criteria and jurisdictions lead to different pricing/access outcomes.

Cancer immunotherapy (Checkpoints Inhibitors): Drugs like pembrolizumab (Keytruda) and nivolumab (Opdivo) have been through both NICE and ICER. ICER’s value assessments for these agents often found them not cost-effective at launch prices, citing incremental cost/QALYs well above $100k (ICER’s upper bound) ([40]). For instance, pembrolizumab (for certain cancers) had an ICER of ~$236k/QALY, beyond ICER’s range ([44]). NICE’s evaluations, by contrast, incorporated sizable discounts under the Cancer Drugs Fund arrangements or PAS. Some NICE appraisals initially recommended use only within the Cancer Drugs Fund (a special UK fund for promising cancer drugs not yet meeting NICE thresholds). Eventually, companies reduced price, and NICE granted full approval in 2023 for pembrolizumab in several indications at negotiated price, while ICER still lists its value-based price about 50% below U.S. price ([12]) ([44]). This reflects the pattern: U.S. price remains at manufacturer’s level (justifying ICER’s moderate-high threshold breach), while UK price is cut to fit budget.

CAR-T cell therapies: Chimeric Antigen Receptor T-cell treatments (e.g. tisagenlecleucel, axicabtagene ciloleucel) famously cost about $400,000–475,000 per patient in the U.S. at launch. ICER evaluated them at launch and concluded they exceed $150k/QALY unless prices fall dramatically or only very few patients are treated ([26]). NICE similarly faced these high values. In 2019, NICE initially did not recommend tisagenlecleucel for pediatric ALL, even though it could be curative, because at £282k (about $350k) it far exceeded UK thresholds . After intense negotiation, Novartis offered an outcome-based scheme and significantly lower NHS price, and NICE gave positive guidance under an Innovative Medicines Fund pathway. AXA/blue coverage in U.S. remained on-hold for about 18 months (with ICER involved in discussions) until manufacturers signed bilateral deals. The lesson: for CAR-T, NICE could force the price down through coverage denial (until it met the threshold), while ICER’s reports strongly signaled the need for discounts, but U.S. payers still paid list prices (often 50% rebates) under individual contracts.

Gene therapies (Luxturna for retinal dystrophy): Spark Therapeutics’ Luxturna (voretigene neparvovec) is a one-time gene therapy priced at $850,000 for both eyes in the U.S. ICER has evaluated similar one-shot cures and typically calculates a “value-based price” somewhat below list (e.g. 40–50% of launch price). In the UK, NICE’s new system of “affordable access” included Luxturna as one of first candidates: NICE, NHSE and NHSCR in late 2023 agreed to fund Luxturna under a commercial deal (the exact price is confidential) ([45]). It is reported that this price was substantially below the U.S. price (one British health economist noted it was “significantly lower”) ([41]). This is consistent with the Parkinson’s model: the UK budget threshold likely necessitated a lower per-patient price. Meanwhile, ICER’s analysis would accept far more per patient under a $150k/QALY criterion, but it too acknowledges the trade-off of fewer patients treated if price must remain low ([14]).

Diabetes/Obesity (GLP-1 agonists): New weight-loss drugs (e.g. semaglutide branded Wegovy) pose different issues. NICE is currently evaluating them for NHS use. Given that the NHS pays <£100 for generic diabetes drugs per month, a therapy costing £1,000/month would typically fail the NICE test unless major benefits attach. Meanwhile, ICER has reviewed analogous obesity drugs (perhaps Lilly’s tirzepatide). At U.S. prices (~$1,000/month), ICER found these near the $150k/QALY threshold for diabetic benefit, but well beyond for obesity alone. If NICE deems a drug cost-effective (likely only at steep discount or with special criteria), it will need NHS negotiations. ICER will likely push for rebates or restrict coverage (as some U.S. payers have done via step therapy). This case demonstrates that even for non-cancer conditions, NICE’s lower price expectations can limit access compared to the U.S. A June 2025 press story noted NICE considers a multi-year appraisal to decide on GLP-1s, mindful of both clinical data and cost (reflecting NICE’s rigor) ([46]). In the U.S., insurers in 2024 applied strict controls (e.g. only covering for diabetic patients at highest BMI), arguably because ICER reported a narrower value window. Thus both agencies act as gatekeepers: NICE via mandated cost-effectiveness, ICER via payer pressures and contracting.

Miscellaneous – Rare Disease and End-of-Life: Drugs for ultra-rare conditions (enzyme replacements, small population gene therapies) highlight differences. NICE’s HST program allowed up to ~£300k/QALY when launched, then restricted to ~£100kとな ([5]). Nevertheless, some orphan drugs (e.g. Strimvelis for ADA SCID) were turned down by NICE until prices fell. ICER tends to value such cures highly given severity (some with minimal QALY denominators), often accepting higher WTP. For example, ICER rated an ultra-rare metabolic therapy as “intermediate value” at $300k/QALY with evLYG accounted ([9]). NICE, under its budget constraints, might have rejected it if it could not secure an extremely low UK price. Despite rising thresholds for ultra-orphans, NICE still must test affordability. This aligns with Jørgensen’s point: even when a cure is “worth” more per patient in the U.S., the UK’s smaller market may pay less per dose to keep overall spending in check ([14]) ([15]).

In each case, the pattern is clear: ICER tends to approve (or say “value for money”) only at higher price points, while NICE often demands a lower effective price to say “yes.” Patients in each system may end up with the same effective coverage (assuming deals are struck), but the distribution of payment is shifted. For example, if a UK doctor can now prescribe drug X, the NHS (taxpayers) is paying less per dose than U.S. insurers would; conversely, the U.S. market price remains higher, allowing recoupment of R&D by the manufacturer while cross-subsidizing the UK discount.

Discussion: Implications and Future Directions

The comparison above reveals how policy architecture shapes drug access worldwide. In strict economic terms, NICE and ICER agree about the basic goal (maximize health per dollar) but differ on who pays and how much they will pay before that equation breaks down.

One clear implication is budgetary discipline versus innovation incentive. NICE’s original £30k/QALY threshold was designed to reflect the average NHS opportunity cost (the health that must be foregone when funding the drug). Over time, critics argued that unchanged thresholds failed to account for inflation or societal willingness to pay more for cutting-edge treatments. The 2025 decision to raise NICE’s range to £25k–35k ([4]) suggests UK policy is moving toward greater emphasis on supporting innovation (at least for now) and alleviating business climate concerns. This means some drugs that would have been borderline may now be accepted at unchanged prices. From a global perspective, a higher NICE threshold could encourage manufacturers to offer somewhat higher UK prices, raising the price “floor” overall. It also indicates a philosophical shift: British policymakers signaled that in a publicly-funded system, extra spending (via tax) on new drugs is justified to unlock more therapies.

ICER’s future direction seems to revolve around method refinement rather than threshold change. Its 2023 update notably left WTP benchmarks ($50–200k) intact, but it introduced more sophisticated handling of non-health benefits, equity, and affordability. ICER signaled interest in incorporating distributional concerns (investigating the GRACE approach to weight severe cases) ([39]) and in quantifying health disparities (via its HIDI index). It also recognized the need to consider in-confidence clinical data more systematically ([47]). If ICER’s framework begins to formally incorporate broader elements of value – or if U.S. payers start demanding a “societal perspective”– its effective thresholds might flex, possibly growing to reflect value of innovation or shrink under cost pressures. Meanwhile, on the policy front, ICER’s influence could intensify: U.S. proposals for Medicare drug price negotiation (e.g. from the Inflation Reduction Act of 2022 onward) were born from the idea that U.S. should pay only a price commensurate with clinical benefit as recognized globally ([16]). ICER could either feed into this (by providing analyses Medicare could use) or face a regulatory limit if government sets a different price path (e.g. linking to global prices without regard to ICER thresholds).

Globally, HTA is becoming a collaborative enterprise. NICE has partnered with many international bodies (Australia’s PBAC, Canada’s CADTH, the newly cooperating European HTA network) ([48]), sharing methods and sometimes co-developing guidance. Likewise, there is increasing talk of international pricing agreements to avoid the “prisoner’s dilemma” of independent negotiations. If, for example, a stable global reference price index were set by treaty or a WHO mechanism, then NICE and ICER thresholds might converge to defend those norms. Conversely, any unilateral stance (like the UK raising threshold or U.S. referencing the lowest price) disturbs global equilibrium.

Another factor is societal preferences. NICE’s Citizens Council and social value judgments indicate the UK public accepts trade-offs: they have historically tolerated NHS co-payments to ensure broad access. ICER publishes its work centuries of think-tank in format but functions similarly to gauge U.S. stakeholders’ views. If national cultures change how they value innovation or equity, NICE and ICER will reflect that. For instance, public demand could push NICE to weight severe disease more (beyond current “end-of-life” rules) or push ICER to accept higher WTP for transformative cures. These shifts would alter the “pricing floors” by letting higher prices pass the value test.

Finally, data and real-world evidence will increasingly shape both agencies’ work. NICE has begun welcoming longer-term real-world outcomes (via managed access) to reassess cost-effectiveness post-launch. ICER has adapted to use any credible unpublished evidence (with safeguards) ([49]). As outcomes-based contracts become more common, both NICE and ICER might incorporate actual performance into their models. If treatments turn out more effective than in trials, their value increases (raising heath or lowering cost/QALY). Underdelivery of benefit or side effects would lower value. This feedback loop will affect future pricing: for example, an approval contingent on future cost-effectiveness (like NICE’s cancer drugs fund) can either confirm or revoke initial pricing.

Conclusion

NICE and ICER represent two sophisticated approaches to assessing drug value. NICE operates within a universal healthcare system, using mandated cost-effectiveness thresholds and enforced price negotiations to balance patient access with NHS affordability. ICER exists in a market-driven system, applying similar analytic rigor but no binding force, effectively offering guidance on what prices society should consider fair. Both have significant indirect influence: NICE by virtue of its central role in the NHS and its effect on international reference pricing, and ICER by shaping U.S. payer decisions and the policy narrative on drug cost.

Empirical evidence indicates that these organizations often reach similar conclusions about the relative value of therapies once price is accounted for: a drug deemed to provide only modest benefit at high cost will be ranked low by both ([12]) ([13]). Where they diverge is typically price. If U.S. prices exceed what NICE would accept, the drug may be approved in the U.S. (especially if ICER’s higher threshold is met) but effectively unavailable (without massive discounts) to UK patients. Conversely, some drugs rejected by ICER may still reach the market if NICE helps lower their price.

Looking ahead, NICE’s raising of its threshold and ICER’s refined frameworks will shift these benchmarks. NICE’s willingness to pay more hints that somewhat higher drug prices (and thus higher global price floors) might become acceptable – at least temporarily in the UK. ICER’s continued use of a high-dollar WTP range reflects and reinforces the premium U.S. pays for innovation, although U.S. policy efforts like international benchmarking threaten to constrain it. The interplay between public HTA and private negotiations will continue to define a sea change in drug pricing policy.

Ultimately, the collaboration and competition between NICE and ICER will help determine the norms of what constitutes “value” in medicine internationally. Stakeholders worldwide—governments, insurers, manufacturers, and patients—must watch both institutions. By understanding their methods and limits, decision-makers can better navigate trade-offs between innovation and affordability. In the context of spiraling drug costs and budget constraints, NICE and ICER are each pivotal reference points: together, they set a global baseline for drug value that shapes markets in London, Boston, and beyond ([12]) ([16]).

External Sources (49)

Need Expert Guidance on This Topic?

Let's discuss how IntuitionLabs can help you navigate the challenges covered in this article.

I'm Adrien Laurent, Founder & CEO of IntuitionLabs. With 25+ years of experience in enterprise software development, I specialize in creating custom AI solutions for the pharmaceutical and life science industries.

DISCLAIMER

The information contained in this document is provided for educational and informational purposes only. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability of the information contained herein. Any reliance you place on such information is strictly at your own risk. In no event will IntuitionLabs.ai or its representatives be liable for any loss or damage including without limitation, indirect or consequential loss or damage, or any loss or damage whatsoever arising from the use of information presented in this document. This document may contain content generated with the assistance of artificial intelligence technologies. AI-generated content may contain errors, omissions, or inaccuracies. Readers are advised to independently verify any critical information before acting upon it. All product names, logos, brands, trademarks, and registered trademarks mentioned in this document are the property of their respective owners. All company, product, and service names used in this document are for identification purposes only. Use of these names, logos, trademarks, and brands does not imply endorsement by the respective trademark holders. IntuitionLabs.ai is an AI software development company specializing in helping life-science companies implement and leverage artificial intelligence solutions. Founded in 2023 by Adrien Laurent and based in San Jose, California. This document does not constitute professional or legal advice. For specific guidance related to your business needs, please consult with appropriate qualified professionals.

Related Articles

Gene Therapy Pricing: The Economics of Million-Dollar Cures

Updated April 2026: Million-dollar gene therapy pricing analysis covering Casgevy, Lyfgenia, Lenmeldy, Elevidys (with 2025 safety update), the Roctavian and Beqvez market withdrawals, and CMS's 2025 Cell and Gene Therapy Access Model. Compares one-time cure costs to lifetime chronic care using value-based pricing, ICER QALY thresholds, and outcomes-based contracts.

QALYs & Quality of Life: Justifying Specialty Drug Costs

Learn how patient quality of life (QoL) data is quantified into Quality-Adjusted Life Years (QALYs) to perform cost-effectiveness analysis for specialty drugs.

QALYs & ICERs Explained: Core Health Economics Metrics

An educational guide to QALYs and ICERs, the core metrics in health economics. Learn how they measure value and guide cost-effectiveness decisions. Updated April 2026 with NICE's new £25k–£35k/QALY threshold.