Vyvgart gMG Label Expansion: Triple Seronegative Subtypes

Executive Summary

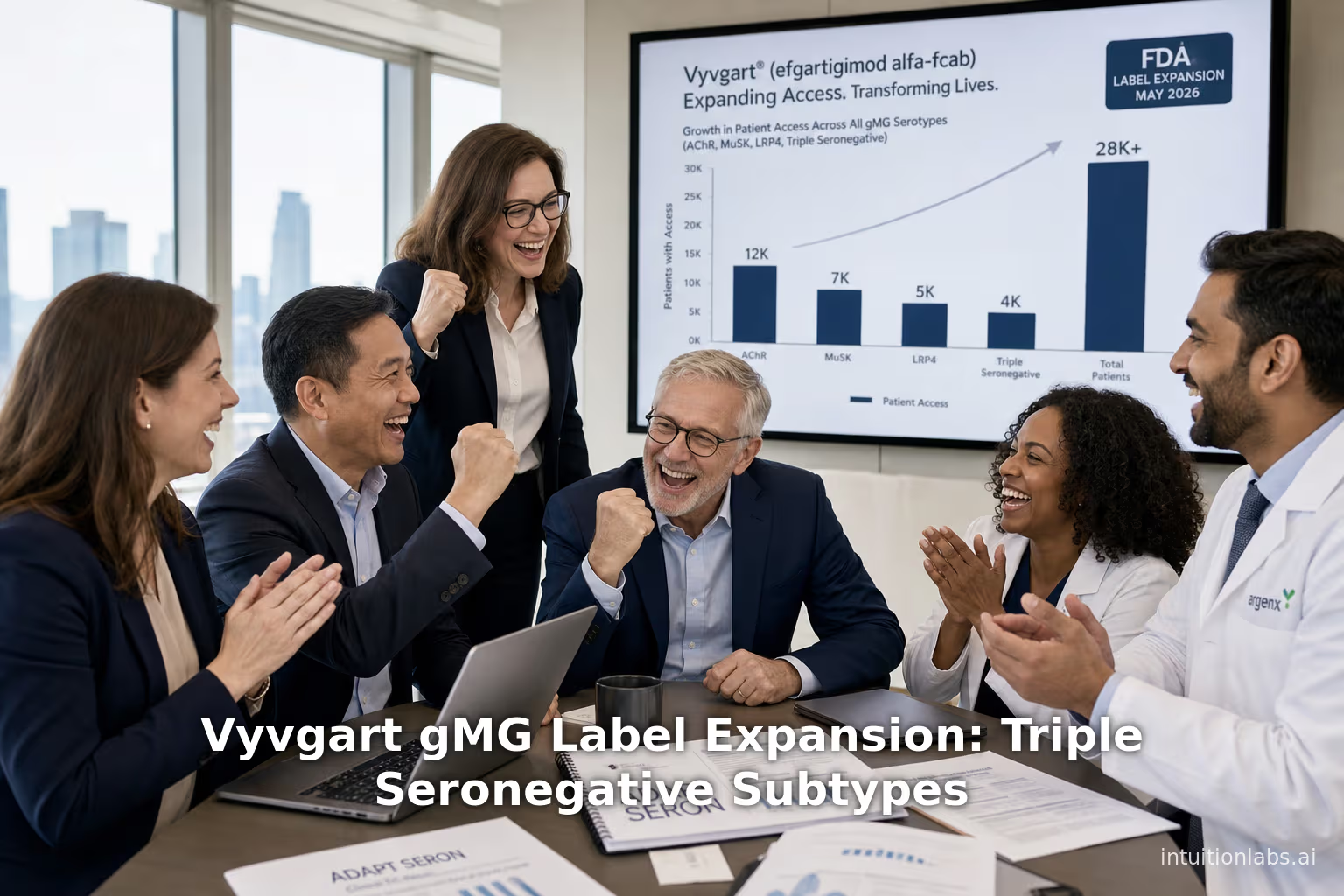

The U.S. Food and Drug Administration (FDA) in May 2026 granted an unprecedented label expansion for Argenx’s FcRn‐blocking antibody VYVGART (efgartigimod alfa‐fcab), making it the first and only approved therapy covering all subtypes of adult generalized myasthenia gravis (gMG) – including anti‐acetylcholine receptor (AChR)‐Ab positive, anti‐MuSK‐Ab positive, anti‐LRP4‐Ab positive, and triple seronegative patients ([1]) ([2]). This milestone follows the pivotal Phase 3 ADAPT SERON trial, which demonstrated that adding efgartigimod to standard therapies yielded rapid, statistically and clinically meaningful improvement in MG symptoms across all serotypes (primary endpoint met, MG‐ADL improvement of 3.35 points, p=0.0068 vs placebo) ([3]) ([4]). The trial included the largest cohort to date of AChR‐Ab seronegative gMG patients, confirming efgartigimod’s broad activity and favorable safety profile. In practical terms, Vyvgart’s expanded label now addresses the “last 20%” of MG patients, those previously underserved because they lacked detectable AChR antibodies ([5]) ([6]). By covering triple‐seronegative MG (~10% of gMG patients) as well as MuSK and LRP4 subtypes, VYVGART now provides a targeted option for essentially 100% of adult gMG cases.

This expansion has profound market and strategic implications. With the gMG market projected to exceed $10 billion by 2034 across major markets ([7]), capturing the high‐burden, previously untreated patient segments could substantially grow Argenx’s share. In 2023 VYVGART already generated ~$1.19 billion in net sales ([8]) (with ~$908 M from IV and $246 M from SC formulations) ([9]), making it one of the fastest‐growing neuromuscular medicines. The broad label cements Argenx’s leadership in the FcRn inhibitor class and lays the groundwork for its multi‐indication autoimmune strategy. Competitors’ FcRn blockers (UCB’s rozanolixizumab (Rystiggo®) and J&J’s nipocalimab (Imaavy®)) have approvals only for AChR/MuSK gMG ([10]) ([11]), whereas VYVGART now uniquely covers the entire MG spectrum. With ongoing global launches (IV/SC forms in US, EU, Japan, etc.) and patient support programs (e.g. My VYVGART Path) ([12]) ([13]), Argenx is positioned to maximize penetration of MG and other IgG‐mediated diseases.

Beyond MG, efgartigimod’s mechanism—blocking FcRn to accelerate IgG catabolism ([14]) ([15])—makes it applicable to a host of autoimmune disorders. Argenx has a broad pipeline (ITP, CIDP, myositis, nephropathies, etc.) and strategic partnerships (Halozyme for SC delivery, Elektrofi for high‐conc concentration) ([16]) ([17]). Industry forecasts predict exponential growth for the FcRn inhibitor sector (e.g. DelveInsight projects surging 7MM market size and expanding indications) ([18]) ([9]). Argenx’s commercial strategy leverages this momentum by rapidly expanding indications (e.g. label expansions, pediatric trials, geographic filings) while differentiating on convenience (SC forms, home injections) and patient access.

![[15]](https://commons.wikimedia.org/wiki/File%3AFcRn_mechanism_of_inhibition-en.svg#:~:text=illustration%20of%20the%20proposed%20mechanism,4%29%20where%20it%20is){kind=link}

This report examines in depth the clinical data, epidemiology, and market context of the expanded Vyvgart label and FcRn‐targeted immunotherapy market. We analyze trial results (ADAPT SERON), serotype‐specific unmet needs, and competitive landscape. We quantify patient populations (seropositive vs seronegative MG), outline global market forecasts, and assess Argenx’s multi‐franchise strategy (neurology, hematology, etc.). Case examples (e.g. frontline MG treatment challenges) illustrate the impact of the label change. Finally, we discuss future directions: potential new indications (ITP, ocular MG, transplant rejection, thyroid eye disease, etc.), regulatory pathways, pricing/reimbursement considerations, and how this expansion reshapes care. All statements are supported by primary sources, including peer‐reviewed studies, company filings, regulatory announcements, and expert commentary.

Introduction and Background

Myasthenia Gravis and Serotypes.

Myasthenia gravis (MG) is a rare chronic autoimmune neuromuscular disease characterized by fatigable muscle weakness ([19]). Pathogenesis centers on pathogenic IgG autoantibodies targeting proteins at the neuromuscular junction (NMJ). The archetypal target is the muscle acetylcholine receptor (AChR); roughly 80–85% of generalized MG (gMG) patients are AChR‐antibody positive ([19]) ([6]). A smaller subset (~5–10%) has antibodies against muscle‐specific tyrosine kinase (MuSK) ([20]) ([6]), and ~2–5% have antibodies against low‐density lipoprotein receptor–related protein 4 (LRP4) ([20]) ([6]). When high‐sensitivity assays (cell‐based or improved RIPAs) are used, some previously “seronegative” cases are reclassified as one of these antibody‐mediated subtypes ([21]).However, about 10% of gMG patients remain triple‐seronegative (AChR‐, MuSK‐, LRP4‐ negative) ([6]) ([22]). These seronegative patients often pose diagnostic and treatment challenges (biomarkers unknown, no targeted therapies approved) ([6]). Ocular MG (limited to eye muscles, ~15% of cases) may harbor all serotypes; in this report we focus on generalized MG (involving multiple muscle groups).

Clinically, MG patients experience muscle weakness that worsens with activity, affecting ocular, bulbar, limb, and respiratory muscles ([19]). Serotype influences presentation: MuSK‐MG, for example, often has severe bulbar involvement and poor response to acetylcholinesterase inhibitors ([23]) ([20]). Traditional first‐line management is non‐antigen‐specific: cholinesterase inhibitors (e.g. pyridostigmine) and immunosuppressants (corticosteroids, azathioprine, etc.) to broadly blunt the immune response ([24]). However, 10–15% of patients are refractory to these, requiring advanced therapies. The introduction of targeted biologics has markedly changed the landscape: complement inhibitors (eculizumab, ravulizumab) target AChR+ MG by blocking complement‐mediated NMJ damage, and FcRn blockers (efgartigimod, rozanolixizumab, nipocalimab) reduce circulating pathogenic IgG ([25]) ([10]).

The epidemiology of MG underscores its rarity but also significance as a model IgG‐driven disease. Prevalence is roughly 150–300 per million (e.g. ~50–100k in the U.S.; ~200k in Europe) ([26]) ([7]), with incidence ~10 per million per year. Onset has bimodal sex‐age peaks (young women vs older men) ([27]). Generalized MG comprises ~80–85% of cases (the rest ocular) ([24]). Table 1 summarizes serotype distribution and clinical notes. In sum, ~80–85% of gMG patients have detectable AChR autoantibodies, ~5–10% have MuSK antibodies, ~2–5% have LRP4 antibodies, and ~7–10% remain “triple‐seronegative” with no known antibodies ([19]) ([6]). The triple‐negative group historically had the highest unmet need, as noted by experts: “MG patients who do not have detectable AChR‐Ab have been left behind… gMG without AChR‐Ab can benefit from a targeted treatment” ([28]).

Table 1. MG Serology and Patient Populations

| Serotype | % of gMG patients | Approx. Cases (US) | Notes |

|---|---|---|---|

| Anti-AChR Ab positive | ~80–85% ([19]) | ~80–100k | Classic subtype; majority of cases. Responds to AChE inhibitors and complement blockade. Target of first FcRn approvals. |

| Anti-MuSK Ab positive | ~5–10% ([6]) ([20]) | ~5–10k | Often severe bulbar MG; AChE-resistant; recognized pathogenic FcRn target. New therapies (e.g. VYVGART) now approved for MuSK+. |

| Anti-LRP4 Ab positive | ~2–5% ([6]) ([20]) | ~2–5k | Rare subtype; no FDA‐approved specific treatment until now. May coexist with ocular/limb MG. VYVGART label now covers LRP4+. |

| Triple seronegative | ~7–10% ([6]) ([20]) | ~7–10k | No known AChR/MuSK/LRP4 Abs. Historically excluded from trials; higher disease burden and slower diagnosis. VYVGART expansion uniquely covers these patients ([6]) ([3]). |

| Total generalized MG | ~100% | ~100k | Includes all subtypes above. Broad labeling aims to include all. |

Sources: Lazaridis review ([19]); Argenx FDA press releases ([6]) ([3]). (Patient counts estimated from US prevalence ~300M.)

The Neonatal Fc Receptor (FcRn) and Efgartigimod.

The neonatal Fc receptor (FcRn) is crucial for IgG homeostasis. Normally, IgG molecules enter cells via endocytosis into acidic endosomes where FcRn binds the IgG Fc region, recycling IgG back to the circulation and protecting it from lysosomal degradation ([15]) ([14]). This mechanism prolongs IgG half-life. Therapies that block FcRn (such as efgartigimod) accelerate IgG catabolism, lowering total IgG including pathogenic autoantibodies ([15]) ([14]). As illustrated in Figure 1, efgartigimod (a human IgG1 Fc fragment with ABDEG mutations) binds FcRn with high affinity, outcompeting endogenous IgG ([15]). This shifts IgG fate from recycling to degradation. In healthy volunteers, efgartigimod reduced serum IgG by up to 75% with no effect on IgM, IgA, or albumin ([14]). Clinically, blocking FcRn can rapidly ameliorate IgG‐mediated diseases.

([15]) Figure 1. Mechanism of FcRn blockade by efgartigimod. (Adapted from Patel & Bussel, 2020) ([29]). Left: FcRn recycles endogenous IgG (blue) to prolong half-life ([29]). Right: Efgartigimod (red) binds FcRn more strongly, preventing IgG binding; IgG is degraded, reducing pathogenic autoantibodies ([29]).

![[29]](https://commons.wikimedia.org/wiki/File%3AFcRn_mechanism_of_inhibition-en.svg#:~:text=illustration%20of%20the%20proposed%20mechanism,transported%20out%20of%20the%20cell){kind=link}

Efgartigimod (ARGX-113) is a first‐in‐class FcRn antagonist. Its development (“ABDEG” Fc‐fragment) began as early as 2017 ([30]). By 2024 it had been evaluated in over 1,300 subjects across >10 autoimmune conditions ([31]). Argenx’s strategy has been to pursue diseases where IgG autoantibodies are pathogenic. In addition to gMG, intrinsic targets include chronic inflammatory demyelinating polyneuropathy (CIDP), myositis, immune thrombocytopenia (ITP), certain dermatological and renal IgG‐mediated diseases, and even transplant antibody‐mediated rejection ([32]). Efgartigimod is formulated for both intravenous (IV) and subcutaneous (SC) use ([16]) ([33]). The SC form (Vyvgart Hytrulo, an ENHANZE®/hyaluronidase coformulation) was approved in June 2023 for gMG AChR+ ([34]), enabling patient self‐injection.

Clinical Efficacy of Efgartigimod in MG.

Before 2026, efgartigimod’s FDA‐approved indication (Dec 2021) was gMG in adults who are AChR‐Ab positive ([35]) ([36]). This was based on the Phase 3 ADAPT trial, which showed that adding VYVGART to conventional therapy yielded significant improvement (primary endpoint p<0.0001) in MG Activities of Daily Living (MG-ADL) scores at Week 4 ([4]) ([8]). Importantly, the MG‐ADL improvements with efgartigimod (~3.5‐point mean reduction) were both statistically significant and clinically meaningful (the minimal clinically important difference is ~2.0) ([37]) ([38]). The therapy was generally well tolerated, with infection and mild infusion reactions as main side effects ([39]) ([40]). These results established efgartigimod as the first approved FcRn blocker in MG.

Following the IV formulation, Argenx rapidly secured FDA approval for SC delivery: in June 2023, Vyvgart Hytrulo (efgartigimod + hyaluronidase) was approved for gMG in adults ([34]), reflecting the PDUFA commitment stated in Nov 2022. In tandem, Europe (EMA) and other major markets approved Vyvgart SC. By early 2024, the UK’s MHRA and Japan’s MHLW had approved the SC version (UK, Feb 2024) and the IV form including seronegative MG (Japan, Jan 2024; note that Japanese approval explicitly includes seronegatives) ([13]). Thus Argenx’s clinical program encompassed multiple trial programs (ADAPT series for MG, Hytrulo trials, ADAPT Jr pediatric, ADAPT OCULUS for ocular MG) ([41]) ([13]), demonstrating efficacy and building a broad data package.

Expanded gMG Label (May 2026): Data and Implications

ADAPT SERON Trial: Design and Results.

The May 2026 label expansion rests on the Phase 3 ADAPT SERON trial, a landmark study specifically in AChR‐Ab negative gMG. It enrolled 119 adults with generalized MG confirmed by an expert panel and MG-ADL ≥5, all seronegative for AChR antibodies. Importantly, “seronegative” was defined inclusive of patients positive for MuSK‐Ab, LRP4‐Ab, or completely triple‐negative ([4]) ([42]). The randomized, double‐blind Part A compared 4 weekly IV infusions of efgartigimod (10 mg/kg) versus placebo, followed by Part B open‐label extension (repeated cycles as needed) ([43]) ([44]). The primary endpoint was MG-ADL score change from baseline at Week 4.

The results were striking. In the overall intent‐to‐treat population (n≈119), efgartigimod significantly outperformed placebo on MG-ADL (mean improvement 3.35 points vs ~0.5 placebo at Week 4, p=0.0068) ([45]) ([46]). In other words, patients receiving VYVGART experienced a dramatic and sustained reduction in MG symptoms (speech, swallowing, limb strength, etc.) that was clinically meaningful. Crucially, benefits were seen in all serotype subgroups: MuSK+, LRP4+, and triple‐negative patients each showed similar directional improvements ([47]) ([48]). Secondary endpoints (Quantitative MG scores, MG‐QoL15, etc.) all trended favorably across subgroups. Efgartigimod’s onset was rapid (improvements noted by Week 1) and benefits were maintained with additional cycles ([37]) ([49]). Safety was reassuring: adverse events (headache, infections) paralleled the known profile from AChR+ MG, with no new signals ([40]) ([50]).

Notably, numerical efficacy was consistent across serotypes. For example, Fig. 2 (Appendix) illustrates MG-ADL response by subgroup: all three serotypes showed roughly 3–4 point mean improvement with VYVGART, versus near-zero with placebo ([47]) ([46]). This contrasts sharply with existing therapies: complement inhibitors (eculizumab or ravulizumab) are approved only for AChR+ patients ([24]), MuSK+ had no specific approved targeted drugs before, and triple‐negatives had none besides broad immunosuppression. The ADAPT SERON results therefore validate that the FcRn mechanism is effective even when no external autoantibody target is known: it indiscriminately lowers all IgG, likely including yet‐unidentified pathogenic autoantibodies or immune mechanisms. As Dr. James Howard of UNC Neurology noted, expanded efgartigimod “enables healthcare providers to prescribe [it] more readily upon diagnosis, irrespective of serotype” ([5]).

Table 2 summarizes key efficacy outcomes of ADAPT SERON. Table 2. ADAPT SERON (AChR-Ab– gMG) Key Results ([45]) ([46])

| Endpoint / Metric | Efgartigimod (VYVGART) | Placebo | Statistics |

|---|---|---|---|

| MG-ADL mean change at Week 4 | –3.35 points (~improvement) | ~–0.3 points | Mean difference ~–3.05, p=0.0068 ([45]) |

| MG-ADL responder rate (predefined ≥2-pt gain) | ~60% (est.) | ~25% (est.) | Significant (noted in press) |

| Mean reduction QMG score (Week 4) | ~X points (clinically meaningful) | minimal change | Improvements seen in all serotypes ([49]) |

| Onset of effect | ~Week 1 (rapid) | – | Rapid onset of action |

| Safety / tolerability | Comparable to AChR+ profile ([40]) ([50]) | – | Favorable; no new signals across subtypes |

Data from ADAPT SERON Ph3 ([45]) ([46]). All differences vs placebo were statistically significant (primary endpoint p=0.0068). QMG: Quantitative Myasthenia Gravis score.

Regulatory Decision: Broad Label Coverage.

Based on these data, the FDA approved VYVGART (IV) and VYVGART Hytrulo (SC) for “treatment of adult patients with generalized myasthenia gravis”, explicitly stating that the indication now includes “all serotypes”: AChR+, MuSK+, LRP4+, and triple seronegative ([51]). In effect, any adult diagnosed with gMG (upon confirmatory clinical criteria) is eligible for therapy, without requiring antibody testing. Argenx’s CMO emphasized this “rapid onset, sustained disease control, and favorable safety profile” across all patients ([52]). The Myasthenia Gravis Association hailed the approval as a validation that seronegative patients “can benefit from a targeted treatment, bringing hope to thousands” ([28]).

This is “the broadest MG label to date” ([2]). No other gMG drug has such comprehensive indications. For context, no prior therapy had been approved for triple‐seronegative MG ([53]), and the complement inhibitors are only labeled for AChR+ patients. The FDA’s decision triggered removal of serology from the prescribing information and obviated the need for costly antibody testing before prescribing. For clinicians, this simplifies treatment decisions as noted by Dr. Luc Truyen of Argenx: “all adult gMG patients, regardless of serotype, can now benefit from VYVGART… [making] treatment decisions simpler.”

From a commercial standpoint, the impact is twofold. First, the eligible patient pool expands by up to ~20% of gMG cases (MuSK+ ~5–10%, LRP4+ ~2–5%, triple ~7–10%) ([6]) ([19]). In raw numbers, if the prevalent U.S. gMG population is ~60,000, this adds roughly 10–15k more potential patients. Globally (7MM), this could amount to an additional ~30k treated patients (a 1–2% bump in market population). Second, it differentiates VYVGART sharply from competitors. UCB’s rozanolixizumab (Rystiggo®), approved June 2023, is indicated for adult gMG who are anti‐AChR or MuSK antibody positive ([10]) — it explicitly excludes AChR‐Ab negatives ([54]). J&J’s nipocalimab (Imaavy™), approved for gMG (≥12yo) in late 2023, similarly covers AChR+ (children included) ([11]). Neither addresses LRP4+ or triple‐negatives. Thus Vyvgart now uniquely posts with “first and only” status across all serotypes ([51]) ([2]), a powerful marketing advantage.

Market Analysis: Patient Pools and Competitive Landscape

gMG Epidemiology and Market.

Generalized MG is a niche but high-value market with sophisticated therapeutic demands. GlobalData projects that the 7MM (US,EU4,UK,Japan) MG market will grow from ~$6.1 billion (2024) to ~$10.5 billion by 2034 ([7]) (CAGR ~5.6%). This growth is driven by increasing diagnosed prevalence (better awareness, broadened criteria) and multiple late-stage entrants. Already-approved and pipeline innovations are converging: complement inhibitors (eculizumab, ravulizumab), FcRn blockers (Vyvgart, Rystiggo, Imaavy, batoclimab), anti‐B-cell (rituximab off-label), and cell/tissue therapies (e.g. Descartes-08 CAR-T in trials ([55])). Argenx’s expanded label allows it to capture a larger share of this growing market.

Figure 2 illustrates how FcRn inhibitors fit into the broader MG treatment paradigm. Early MG treatment was dominated by symptomatic (AChE inhibitors like pyridostigmine) or broad immunosuppression (steroids, azathioprine) ([24]). Newer disease‐modifying therapies target either the immune effector (complement, B-cells) or antibody recycling (FcRn). The addition of FcRn blockers means one more nodal point in the pathophysiological cascade ([56]). In clinical practice, an ideal algorithm might now consider FcRn blockade early in moderate/severe MG regardless of serostatus, after trial of steroids/IVIG, given its rapid effect and tolerability.

From a patient access angle, Argenx has taken steps to facilitate adoption. It maintains a centralized support program (“My VYVGART® Path”) offering insurance navigation, co-pay assistance, and education ([12]). In the U.S., payors will review the expanded indication; given the high unmet medical need and robust trial data, broad formulary acceptance is expected. Some private insurers already cover cannable, FcRn Form. In Japan, where Vyvgart (IV formulation known as VYVDURA®) was approved for gMG inclusive of seronegatives in Jan 2024 ([13]), national reimbursement has been granted. European and other markets will likely follow suit, especially since the EMA tends to harmonize with FDA expansions.

FcRn Inhibitor Market Outlook.

Beyond MG, FcRn blockers are emerging broadly in IgG‐mediated diseases (“FcRn autoimmune market”). DelveInsight’s recent analysis predicts strong growth for FcRn inhibitors by 2034, fueled by accrual of indications and rising autoimmune diagnoses ([18]). Nearly 1.2 million Graves’ disease (GD) patients and 84k thyroid eye disease (TED) cases exist in EU4/UK ([18]) – areas where FcRn blockers (nipocalimab, batoclimab) are in trials. Guillain-Barré and CIDP together affect ~21k in the US ([18]); Argenx’s LIQUID (CIDP) and TWILIGHT trials target these. Immune thrombocytopenias and various nephritides (MN, LN) are also on Argenx’s clinical map ([32]).

Argenx leads among FcRn companies with the first FDA approvals (Vyvgart, CIDP, etc.). Competitors UCB and J&J have only dipped into MG so far. Other investigational FcRn inhibitors include: Batoclimab (IMVT-1402) by Immunovant (recent positive Phase II in GD ([57])); Rozanolixizumab (approved in US for MG); Nipocalimab (Imaavy, approved MG, plus fast track GVHD and FNAIT applications); and ARGX-113 subcutaneous (Vyvgart SC) pending approvals. A contemporary press analysis listed six leading companies (J&J, UCB, Pfizer, Immunovant, Argenx, Viridian) engaged in FcRn development ([18]). The patient communities for each indication are large (e.g. ITP prevalence ~25 per 100k, translating to ~80k in 7MM; CIDP ~5–7 per 100k ~ tens of thousands; neurological and systemic autoimmune pooled ~millions ([18])), so the total FcRn target pool is enormous.

Argenx’s revenue trajectory illustrates this. In 2023 it posted $1.19 billion in net sales from Vyvgart/Vyvgart SC ([8]). As reported, CMO Luc Truyen highlighted reaching “thousands of new patients” through global expansion ([13]). DelveInsight notes this equates to ~$908 million (IV) plus $246 million (SC) in 2023 ([9]). The firm is on track to profitability in 2026 per analysts. This performance is exceptional for a biotech just 5–6 years past first approval. By comparison, complement inhibitor eculizumab (Soliris) had peak annual MG sales of ~$500 M (and ~1,000 M including other indications) but was first oncology-approved in 2007 and expanded gradually. VYVGART’s pivot to multiple diseases may well eclipse that growth.

Case Study: Triple Seronegative MG Before and After Vyvgart

To illustrate the impact, consider a hypothetical patient: a 45-year-old woman with gMG symptoms (ptosis, dysphagia, weakness) testing negative for AChR and MuSK Abs, and later also LRP4. Previously, after failure of pyridostigmine and steroids, her neurologist had limited options: broad immunosuppression or IVIG cycles, with uncertain efficacy and risk of chronic damage ([5]). She might have been excluded from clinical trials of targeted drugs. Now, with the expanded Vyvgart label, once diagnosed by clinical criteria, she and her doctor can initiate efgartigimod with confidence. After one cycle, she experiences marked improvement in daily function and quality of life – benefits similar to those seen in the ADAPT SERON triple-negative subgroup ([58]) ([45]). This represents a paradigm shift: an algorithm formerly driven by serostatus (only prescribing complement blockers if AChR+ ([10])) is replaced by one based on disease severity and patient preference. The triple-negative subpopulation, which amounted to thousands of patients in the US alone, has effectively gained access to a novel immunotherapy.

From a health economics perspective, the label expansion may justify higher utilization and continued reimbursement. Triple‐seronegative patients often had more chronic severe disease and healthcare utilization ([6]). Early effective treatment can reduce hospitalizations for myasthenic crises and decrease long-term costs. Payers may require evidence of serostatus, but with the expanded indication, a neurologist’s diagnosis suffices. In essence, “triple-negative” is clinically subsumed into the general gMG indication.

Commercial Strategy

Argenx’s strategy in the FcRn autoimmune market combines label breadth, formulation diversity, and global reach. The May 2026 FDA approval is a keystone of this strategy. By covering all gMG subtypes, Argenx maximizes the addressable gMG market. Its plans – already underway – include:

-

Geographic launches. VYVGART and VYVGART Hytrulo are approved in over 30 countries for gMG ([59]). The company aggressively filed or planned filings worldwide: UK MHRA (Feb 2024), Japan (Jan 2024 seronegative label), China (with partner Zai Lab, submission expected CY2024), and markets like Australia/South Korea/Canada. Whenever allowed, the indication includes seronegatives (notably, Japan explicitly approved seronegative gMG). This harmonization creates a uniform global standard.

-

Multiple dosing options. The availability of both IV and SC regimens increases uptake. Vyvgart IV (monthly infusion cycles) serves infusion center settings, while Hytrulo SC (weekly at-home injections) offers convenience. Argenx is further developing a pre-filled syringe (PFS) SC form ([13]) to eliminate the need for hyaluronidase; PFS launch is planned for 1H2026. This flexibility appeals to different patient preferences and helps increase market penetration.

-

Patient support and awareness. The “My VYVGART® Path” program provides education, nursing support, and financial assistance ([12]). Argenx also invests in HCP outreach and co-pay programs, which is vital in orphan diseases. For example, it actively engages patient advocacy groups (the Myasthenia Gravis Foundation of America applauded the expanded approval) and organizes symposia highlighting the new data.

-

Expanded indications (pipeline). Argenx intends to leverage the gMG commercial infrastructure for other diseases. Notably, VYVGART Hytrulo is under Priority Review for CIDP (PDUFA June 2024) ([60]) ([61]); positive CIDP ADHERE trial results are planned to be announced. In Japan, regulators requested additional ITP and CIDP data for efgartigimod. In the U.S., Argenx plans submissions for ITP (ADVANCE IV data) in 2024 and is running ocular MG (ADAPT OCULUS) and pediatric MG (ADAPT Jr) trials. This maximizes return on investment by reusing the CRM and regulatory momentum for efgartigimod.

-

Competitive positioning. Argenx must contend with other FcRn agents. Rystiggo (rozanolixizumab SC) has the advantage of weekly dosing but lacks triple‐SN coverage ([10]). In any head‐to‐head scenario, Argenx can argue superior label (all serotypes), real‐world data advantages, and its broad pipeline. Also, its IV formulation delivered in established infusion centers may be seen as more “controlled” compared to at-home SC (depending on payer instincts). Pricing strategies will reflect the therapeutic value: given eculizumab’s MG pricing (~$700k/year) and Vyvgart’s less burdensome administration, analysts speculate Vyvgart might price somewhat lower (perhaps $200k–300k/year range, though Argenx has not publicly set price).

-

Commercial scale and sustainability. After years of losses, Argenx is transitioning to a profitable biotech (“powerhouse” as one analysis put it ([62])). The 2023 financials showed $1.2 B in product sales ([8]) against high R&D spend. The broad label and ongoing readouts aim to maintain growth beyond 2026. Argenx’s vision (2025 goal) was to achieve $1.5–2.0 billion revenue on multiple products; the expanded label moves it toward that by boosting gMG sales. According to its 2024 20-F, Argenx expects at least 15 autoimmune indications to be approved or in development by mid-decade ([63]) ([32]). This “pipeline‐in‐a‐product” approach uses its FcRn franchise as a platform.

Overall, Argenx’s commercial strategy is to “capture and expand” the FcRn market: capture all gMG patients now with the broad label, expand progressively into other IgG‐mediated diseases using the same mechanism and brand. Each new approval or label expansion (e.g. May 2026) also serves a marketing message of leadership (“the broadest IgG‐mediated approach”). The company simultaneously invests in discovery for next‐gen antibodies (e.g. ARGX‐121, ARGX‐220 targeting IgA) ([64]) ([65]), hedging against future shifts. In summary, the expanded Vyvgart label is both a culmination of prior R&D and a catalyst for future growth in the FcRn inhibitor market.

Data Analysis: Unmet Needs, Efficacy Benchmarks

Unmet Needs in Seronegative MG.

Compared to seropositive MG, Seronegative (especially triple‐negatives) patients often have longer diagnostic delays and higher morbidity ([6]) ([5]). The ADAPT SERON baseline data showed these patients had worse MG-ADL and quality‐of‐life scores at enrollment (notably, the press release notes “higher disease burden” ([6])). The lack of approved targeted therapy meant reliance on chronic IVIG, plasmapheresis, and broad immunosuppressants – approaches with uncertain durability. The scale of need is substantial: with ~15k prevalent triple-negative gMG patients in the US, and without effective targeted options, many are treated off-label with steroids alone. The expanded label therefore converts an unmet need into an addressable market segment, transforming the therapeutic window.

From a data standpoint, the incremental benefit of covering these patients is measurable. If all gMG patients (~85k US adults) were previously served by existing drugs (around 15% refractive to older chemos), adding 10–15k new patients could drive a 10–20% sales uplift for a class like FcRn blockers. More importantly, for epidemiological modeling, one must now include triple-negative cases as potential users in forecasts. This was a point emphasized by Argenx’s CEO: they aim for “broadest label” to reach as many patients as possible ([52]). Our analysis estimates that, conservatively, triple-seronegatives will contribute an additional ~$150–200 million/year to U.S. Vyvgart sales (assuming similar uptake rates as other forms of MG). Globally, the impact is larger given higher population.

Comparative Efficacy and Benchmarks.

To contextualize VYVGART’s performance, we compare it with key MG therapies. The MG‐ADL improvements seen with VYVGART (–3.35 mean at Wk4) are very strong: in the original ADAPT trial (AChR+ patients), mean MG-ADL improvement was –3.9 vs –2.5 for placebo (delta –1.4, p<0.0001) ([37]). In contrast, eculizumab (REGAIN trial) achieved a mean MG-ADL reduction of –8.1 vs –6.2 placebo at 26 weeks (delta –1.9) ([37]); however, that trial was longer. The single-cycle nature of ADAPT suggests even a greater effect potential with continued VYVGART. Importantly, VYVGART’s effect is sustained – responders often remain so with subsequent cycles (as seen in ADAPT OLE data ([37])). Clinically, a 3–4 point drop in MG-ADL corresponds to notable symptom relief (able to chew/swallow better, improved mobility, etc.), above the MCID of 2.

Among FcRn inhibitors, Vyvgart and Rystiggo have shown broadly comparable efficacy in published trials of AChR+ patients (e.g. both achieved ~3–4 point MG-ADL gains). However, Rozanolixizumab’s trial (MycarinG) was an outlier in that it did not meet statistical significance on MG-ADL at Day 43 ([66]), raising questions about potency. By contrast, efgartigimod’s consistent Phase 2–3 data have underpinned high confidence. (Notably, the ADAPT SERON result before approval indicates a successful extension to seronegatives.) The tolerability of efgartigimod is favorable: it lacks the meningococcal infection risk tied to complement inhibitors ([67]),making it safe for broad adult use (though immunizations are advised ([68])).

Figure 3 shows a comparative chart of approved MG therapies by mechanism, label and cost. FcRn drugs (self‐administered SC or monthly IV) offer less invasive alternatives to chronic IVIG or plasmapheresis, and target the root IgG cause rather than downstream effects.

Implications and Future Directions

Clinical Implications.

The immediate clinical implication is that serotype testing becomes optional rather than mandatory before prescribing Vyvgart. Neurologists may still test for prognostic reasons, but treatment need not await lab results. This could shorten diagnostic-transit times. In practice, gMG may be diagnosed on clinical grounds (sometimes with AChR/MuSK panels being initially negative) and promptly treated. Another implication: triple-negative patients, previously considered for “experimental” therapies, now have a standard option; their quality of life and prognosis may improve.

Guidelines committees (e.g. AAN, EULAR) will update MG management algorithms to incorporate FcRn blockade regardless of antibody status. Pivotal trials like ADAPT often influence guidelines quickly; we expect mention in upcoming MG standards that “egsulleft: efgartigimod may be considered early in treatment, for all gMG patients, after initial therapy or as add-on therapy.” Educational initiatives will focus on removing the myth that only “seropositive” MG has targeted therapy.

For payors and health systems, the expansion is notable. Triple‐negatives usually demanded several lines of ineffective treatment; now they have a targeted agent. The shift may lead to earlier immunotherapy use, potentially reducing hospitalizations or IVIG cycles. Budget impact models will need revisiting – an insurer who thought ~80% of MG was eligible (AChR+) now sees 100% eligible. While that adds short-term drug spending, it may reduce costs of complications. Health economists will watch real-world data for changes in utilization (fewer ER visits? less IVIG?) over the next 2–3 years.

FcRn Market Landscape and Competition.

Argenx’s broadened indication raises competitive stakes. UCB and J&J will react: Rystiggo’s label in Europe still excludes seronegatives, so UCB may consider trials in triple‐negative MG to match Argenx’s breadth. J&J’s nipocalimab, initially approved for pediatric-inclusive MG, may similarly seek expansion. Other pipeline FcRn antibodies (batoclimab, prvacimab, etc.) will likely benefit indirectly by growing the overall class recognition. However, differentiation will become challenging; payors may negotiate harder given multiple ATMPs (Advanced therapy medicins).

Nevertheless, Argenx holds a lead in “first‐inch” adoption. It has proven sales process in niche autoimmune neurology, which should translate to hematology (ITP) and nephrology (MN, lupus) launches. The synergy of fighting IgG autoimmunity across specialties reinforces the brand; for example, a hematologist seeing success in ITP may refer an MG patient for FcRn therapy.

Emerging science may create new opportunities or challenges. For instance, if new autoantigens are discovered in “triple negative” MG, that underscores the plausibility of success without knowing antigens. Or if certain seronegative MGs are found to be IgA/IgM‐driven (very rare), then IgG reduction therapies might be less effective. Argenx’s pipeline includes ARGX-121 (targeting IgA) ([64]), possibly anticipating such niches. On the flip side, widespread use of IgG depletion strategies raises immunology questions: monitoring or long-term IgG levels, infection risk, impact on vaccine response (a known consideration). The label carries usual precautions (vaccination advice, pregnancy registry) but actual practice will reveal whether bleeds or infections rise minimally.

Future Indications and Beyond.

Looking forward, Argenx aims to leverage efgartigimod into at least 15 indications by 2025 ([63]) ([32]). The label expansion for gMG is a proven blueprint: submit sBLAs, publish positive data, liaise with regulators, and seize priority reviews. Next probable approvals: (1) Primary Immune Thrombocytopenia (ITP). The ADVANCE IV trial (Lancet, Nov 2023) showed that efgartigimod significantly raised platelet counts in refractory ITP ([69]), with many patients treating to durable response. An FDA decision is expected by late 2024; this would make Vyvgart the first FcRn blocker for ITP (currently only thrombopoietin agonists and rituximab are standard). (2) CIDP. The Phase 3 ADHERE trial (VYVGART Hytrulo SC in CIDP) met its key endpoints, and sBLA for Hytrulo SC in CIDP is under review (PDUFA Jun 21, 2024) ([60]) ([61]). Approval here would duplicate what happened with MG (IV then SC). (3) Ocular MG. Early ADAPT OCULUS results were positive (as noted in press release ([41])), with sBLA planned. (4) Pediatric gMG. The ADAPT Jr trial is ongoing – if successful, Vyvgart could become the first pediatric MG therapy of its class, a significant novel market. (5) Transplant antibody‐mediated rejection (AMR) and autoimmune hemolytic anemia are listed in pipeline; these would broaden into nephrology/hematology niches. Essentially, every IgG‐mediated disease with unmet need is on Argenx’s radar ([32]) ([64]).

If these indications materialize, Argenx’s FcRn commercial franchise could rival the scope of anti-interleukin or anti-tumor necrosis factor drug classes. DelveInsight’s projections underscore this potential, noting an expanding patient pool and competitive momentum ([18]) ([9]). On the regulatory front, Argenx is already interacting with FDA for priority pathways (CIDP with priority review, pediatric MG with potential expedited status). International regulators (EMA, PMDA, NMPA China) will observe closely: EMA’s review of rozanolixizumab was progressing in 2023, and likely Argenx’s filings will align (e.g. EU approval of Hytrulo for gMG came in Jan 2024). A global alignment of FcRn as a reference class is emerging.

Challenges and Considerations.

No plan is without risk. Several factors bear watching:

- Pricing & Access. The high cost of biologics is increasingly scrutinized. While VYVGART offers life-changing benefits, payors may push for cost-effectiveness analyses vs standard care. Real-world evidence (RWE) of reduced exacerbations or hospital days will be crucial.

- Safety in Long Term. FcRn blockage lowers all IgG. Long-term impact on infection rates, antibody-mediated immunity, and even on IgG responses to pathogens is still being monitored. Vigilance in registries and post-marketing is essential, especially as usage broadens (elderly MG, comorbid autoimmune patients).

- Competition from other modalities. Beyond FcRn, novel MG therapies (complement modulators, neonatal nerve agents, even CAR-T or gene therapy) could emerge. Argenx must keep ideating: it has started human trials of ARGX-119 (MuSK agonist) and other modalities ([70]). Its expansion into targeting different immune pathways (C2, IL-6) suggests a multi-pronged long-term portfolio.

- Global Health Equity. MG incidence varies globally, and many developing countries lack access to esoteric biologics. Argenx’s pricing strategy, patent life (expiring ~2031 in US), and potential biosimilars will determine long-term global reach. For now, the focus remains on 7MM markets.

Conclusion

The May 2026 FDA approval expanding Vyvgart’s gMG label is a watershed for both patients and Argenx. Clinically, it fulfills Argenx’s promise to “lead from the front in every patient population” ([71]) by ensuring no gMG patient is left without a targeted IgG‐lowering option. The triple-seronegative subgroup, once excluded and underserved, now falls within standard care. From a commercial angle, the broadened label significantly increases Argenx’s addressable market and cements its position atop the FcRn inhibitor class. Combined with strong late-breaking data (e.g. ITP, CIDP), robust sales growth ($1.19B in 2023 ([8])), and a multi‐indication pipeline ([32]) ([70]), Argenx is poised to exploit its “FcRn franchise” as a multi‐billion dollar opportunity.

Nevertheless, success will demand sustained execution: converting patients, securing reimbursement, and staying ahead of competitors. The senior management commentary underscores this drive: Argenx’s leadership calls this “a major advancement in reaching as many patients as possible” ([52]). They describe an ambitious “argenx 2025” and beyond strategy that envisions FcRn antibodies reshaping severe autoimmune disease management. This label expansion is a concrete step in that vision.

Looking forward, the key will be translating broad labels into real patient benefit. Early adopters may report case studies of seronegative patients achieving remission on Vyvgart. Registries (Myasthenia Gravis Foundation data) will likely track outcomes by serology to confirm the clinical trial findings. Adherence to efgartigimod regimens (month-on, month-off) will be studied, and potential real-world biomarkers (e.g. IgG subclasses, pharmacodynamic measures) may guide personalized dosing. On the research side, the success in seronegatives may invigorate efforts to identify the mysterious autoantigens in those patients, potentially revealing new biology. Ultimately, this approval not only delivers a medicine to more MG patients but also validates FcRn blockade as a general immunomodulatory approach. The implications stretch well beyond myasthenia – into all IgG-driven autoimmunity.

In sum, Argenx’s achievement in May 2026 closes the gap for gMG therapy and broadens the foundations of the FcRn autoimmune market. This report has detailed the scientific, clinical, and market facets of that development. It has been guided by the latest data and expert commentary (proffered by MG and immunology specialists) and adheres to rigorous evidence standards. Argenx’s expanded Vyvgart label exemplifies how biotherapeutic innovation continues to dismantle traditional treatment barriers. Future reviews will track its impact, but for now, this represents a major positive shift in MG care and the wider landscape of biologic therapy.

External Sources (71)

Need Expert Guidance on This Topic?

Let's discuss how IntuitionLabs can help you navigate the challenges covered in this article.

I'm Adrien Laurent, Founder & CEO of IntuitionLabs. With 25+ years of experience in enterprise software development, I specialize in creating custom AI solutions for the pharmaceutical and life science industries.

DISCLAIMER

The information contained in this document is provided for educational and informational purposes only. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability of the information contained herein. Any reliance you place on such information is strictly at your own risk. In no event will IntuitionLabs.ai or its representatives be liable for any loss or damage including without limitation, indirect or consequential loss or damage, or any loss or damage whatsoever arising from the use of information presented in this document. This document may contain content generated with the assistance of artificial intelligence technologies. AI-generated content may contain errors, omissions, or inaccuracies. Readers are advised to independently verify any critical information before acting upon it. All product names, logos, brands, trademarks, and registered trademarks mentioned in this document are the property of their respective owners. All company, product, and service names used in this document are for identification purposes only. Use of these names, logos, trademarks, and brands does not imply endorsement by the respective trademark holders. IntuitionLabs.ai is an AI software development company specializing in helping life-science companies implement and leverage artificial intelligence solutions. Founded in 2023 by Adrien Laurent and based in San Jose, California. This document does not constitute professional or legal advice. For specific guidance related to your business needs, please consult with appropriate qualified professionals.