Global Pharmaceutical Market: 2025 Analysis & Key Trends

[Revised July 10, 2026]

Executive Summary

The global pharmaceutical industry is on track to reach unprecedented scale, with spending projected to hit approximately $1.6 trillion by 2025. This figure – which excludes the one-time surge from COVID-19 vaccines – reflects a steady compound annual growth rate (CAGR) of roughly 3–6% from pre-pandemic levels, according to IQVIA Institute forecasts ([1]). The year 2023 already saw global pharmaceutical revenues around $1.6 trillion, up by over $100 billion from 2022 ([2]), underscoring the industry’s robust growth trajectory even amid recent disruptions. By 2024, the worldwide pharma market (including prescription and over-the-counter drugs) was valued at roughly $1.7 trillion, with U.S. prescription drug sales alone contributing about $800 billion – nearly half of global pharma spending ([3]).

Multiple drivers underpin this growth. These include rising global demand for medications driven by aging populations and the increasing burden of chronic diseases (such as cancer, diabetes, and cardiovascular conditions), as well as continual advancements in medical science and biotechnology. The last decade has seen a surge of high-impact innovations – from monoclonal antibodies and immunotherapies to the advent of mRNA vaccines – which have expanded treatment possibilities and opened lucrative new markets. Oncology (cancer) and immunology (autoimmune and inflammatory diseases) have firmly established themselves as the top therapeutic areas by expenditure, each expected to grow around 9–12% annually through 2025 ([4]). IQVIA projects global spending on oncology drugs will reach roughly $273 billion in 2025, with immunology drugs (for conditions like rheumatoid arthritis, psoriasis, and other immune-mediated diseases) close behind at $175 billion ([4]). Metabolic diseases (notably diabetes and the emerging anti-obesity market fueled by GLP-1 analogues) and neurological disorders are also major growth areas, each projected in the mid-$100 billion range by 2025 ([4]).

The industry landscape is being reshaped by a number of key trends and shifts:

-

Regional Dynamics: The United States remains the single largest national pharma market, accounting for an outsized share of global spending (around 50% of the total by value in the mid-2020s) due to high medicine prices and broad access to new therapies ([3]). China is the second-largest market and continues to expand rapidly, though it constitutes a much smaller slice (~8–12% of global sales by varying estimates) reflecting both its aggressive cost controls and the focus of data on hospital drug purchases ([3]). Emerging “pharmerging” markets – a group including large developing economies such as China, India, Brazil, Russia, Turkey, and others – are collectively driving a significant portion of incremental growth. IQVIA estimates that pharmerging markets will contribute around $140 billion in increased spending by 2025, as broader healthcare access and economic growth in those countries lead to greater medicine usage ([5]). Meanwhile, growth in traditional developed markets (North America, Western Europe, Japan) is slower, tempered by loss of exclusivity (LOE) on major drugs and intensifying cost controls. The European Union and Japan face flat or modest growth due to strict price regulation and, in Japan’s case, regular price cuts, even as they adopt new therapies. In 2025, Europe’s medicine spending is expected to grow only ~2–5% CAGR (adding ~$35 billion over five years), and Japan’s market is forecast to be flat or slightly declining due to biennial price reductions and policies promoting generics ([1]).

-

Therapy Area Shifts: Specialty medicines – advanced therapies often for complex or rare conditions (including biologics, targeted therapies, and personalized medicines) – are increasingly dominating expenditure. By 2025, specialty drugs are projected to account for roughly 50% of global pharmaceutical spending, and as much as 60% in developed markets ([5]). The ongoing biologics revolution is a major factor: biologic drugs (such as antibodies, recombinant proteins, and cell/gene therapies) already comprise a large share of top-selling products and are expected to represent over half of global pharma value by 2030 (57% by value, and over 70% of the top 100 product sales) ([6]). This has brought tremendous clinical benefits (for example, immunotherapies transforming cancer care, or enzyme replacement therapies for rare diseases) and high market value, but also ushers in new challenges in manufacturing, pricing, and patient access. Oncology stands out as the largest and fastest-growing segment: global oncology spend has seen double-digit annual growth for the past decade and is on pace to exceed $260 billion in 2025 ([4]). Autoimmune and inflammatory diseases (the immunology segment) are also expanding rapidly with successive waves of novel biologics (e.g. cytokine inhibitors like IL-23 or IL-4/13 blockers) – though this area will soon face a slow-down due to biosimilar competition against aging blockbusters like Humira. Metabolic disease treatments, particularly the glucagon-like peptide 1 (GLP-1) class for type 2 diabetes and obesity, have emerged as a transformational market in the mid-2020s. Remarkably, four GLP-1 based therapies are projected to rank among the world’s top 10 best-selling drugs in 2025, led by Novo Nordisk’s semaglutide (branded as Ozempic for diabetes and Wegovy for obesity) and Eli Lilly’s tirzepatide (Mounjaro for diabetes, recently also approved as Zepbound for obesity). These two drugs alone are expected to generate over $70 billion in combined sales in 2025 ([7]), signaling an unprecedented commercial success and medical impact in metabolic health. Other fields like neurology are also gaining momentum, with new therapies for migraine, multiple sclerosis, and potentially Alzheimer’s disease (e.g. anti-amyloid antibodies) offering hopes for growth in a historically challenging area. By 2025, neurology expenditures could reach ~$140+ billion as innovative treatments for neurological conditions enter the market ([4]).

-

Pipeline Innovation and R&D: The pharmaceutical sector’s engine of growth is its research and development (R&D) pipeline. Across the industry, R&D investment now exceeds $200 billion per year ([8]) – an all-time high – and the output of new therapies is correspondingly high. Between 2021 and 2025, an estimated 290 to 315 new active substances (NASs) will be launched globally (averaging 55–60 new drug launches each year) ([9]) ([10]), a historically elevated rate of innovation. Many of these are specialized drugs targeting smaller patient populations (for example, rare diseases or biomarker-defined subgroups of common diseases), reflecting an industry shift from the traditional one-size-for-all “blockbuster” model to more precision medicine approaches. Notably, orphan drugs for rare diseases have proliferated: in recent years roughly 40–50% of new medications approved by the FDA have been for orphan or rare disease indications ([11]). This trend has been spurred by incentives (regulatory and commercial) and by scientific advances in genetics and biotechnology that allow targeting of niche conditions. The flip side is that many of these therapies come with very high price tags due to small patient pools, raising new questions about affordability.

-

Role of Biotech and Collaboration: A striking development over the past two decades is the increasing role of small biotech firms in drug innovation.Studies show that biotech companies (often venture-funded startups or mid-size biopharmas) have outpaced large pharmaceutical companies in creating breakthrough therapies. For instance, between 1998 and 2016, biotech-originated projects produced 40% more FDA-approved “priority” drugs than the entire big pharma sector, despite biotech spending less than half as much on R&D in aggregate ([12]). This highlights how nimble, science-focused biotech enterprises have become key sources of innovation (especially in cutting-edge areas like gene therapy, CRISPR gene editing, CAR-T cell therapy, and mRNA technology). In response, large pharmaceutical companies have increasingly adopted open innovation models – sourcing compounds and technology externally via partnerships, licensing deals, and acquisitions. In fact, a significant share of new drugs marketed by big pharma in recent years originated in smaller biotech, only later being licensed or acquired. The industry has seen record levels of mergers & acquisitions (M&A) as big players seek to replenish their pipelines and therapeutic portfolios (for example, Bristol Myers Squibb’s $74 billion acquisition of Celgene in 2019 to boost its oncology and immunology pipeline, or Pfizer’s proposed $43 billion acquisition of Seagen in 2023 to expand in cancer immunotherapy). This collaborative ecosystem blurs the line between “biotech” and “pharma,” as many large firms invest in early-stage biotech ventures or form strategic alliances to co-develop drugs.

-

Top Industry Players: Despite the broadening innovation base, the global market remains partly concentrated among leading corporations. The top 10 pharmaceutical companies account for roughly 40% of global pharma sales ([8]). These include a mix of U.S.- and Europe-headquartered multinationals that have long dominated by revenue. As of 2022, the largest pharma company by revenue was Pfizer, which reached an unprecedented $100 billion in sales driven by its COVID-19 vaccine (Comirnaty, developed with BioNTech) and oral antiviral (Paxlovid) ([13]). Other top players include Johnson & Johnson (over $94 billion total revenue in 2022, across pharmaceuticals, medical devices, and consumer health divisions), Roche (~$66 billion, with leadership in oncology and diagnostics), Merck & Co. (~$59 billion, bolstered by the blockbuster cancer drug Keytruda and vaccines like Gardasil), and AbbVie (~$58 billion, largely from immunology drugs like Humira, Skyrizi, and Rinvoq) ([13]). Other companies rounding out the top ten include Novartis (Switzerland), Bristol Myers Squibb, Sanofi (France), AstraZeneca (UK/Sweden), and GSK (UK), each with annual revenues in the $35–50 billion range ([13]). It is worth noting that 2021–2022 temporarily shuffled rankings as COVID-19 vaccine producers (Pfizer, Moderna, etc.) saw spikes in revenue – Pfizer’s 2022 sales, for example, were nearly double its pre-pandemic level – but these are expected to normalize post-pandemic. Nevertheless, the competitive landscape is dynamic; companies’ fortunes rise and fall based on product launches or patent expiries. For instance, Merck’s Keytruda (an immuno-oncology therapy) is the world’s top-selling drug currently (projected >$30 billion in 2025 sales) ([7]), but its main patent expires in 2028, at which point a precipitous decline is anticipated if biosimilar competition emerges. Industry leaders are therefore racing to diversify portfolios and invest in the next generation of therapies, including hot areas like obesity treatments, gene therapies, and neuroscience, to sustain growth beyond the looming patent cliffs.

-

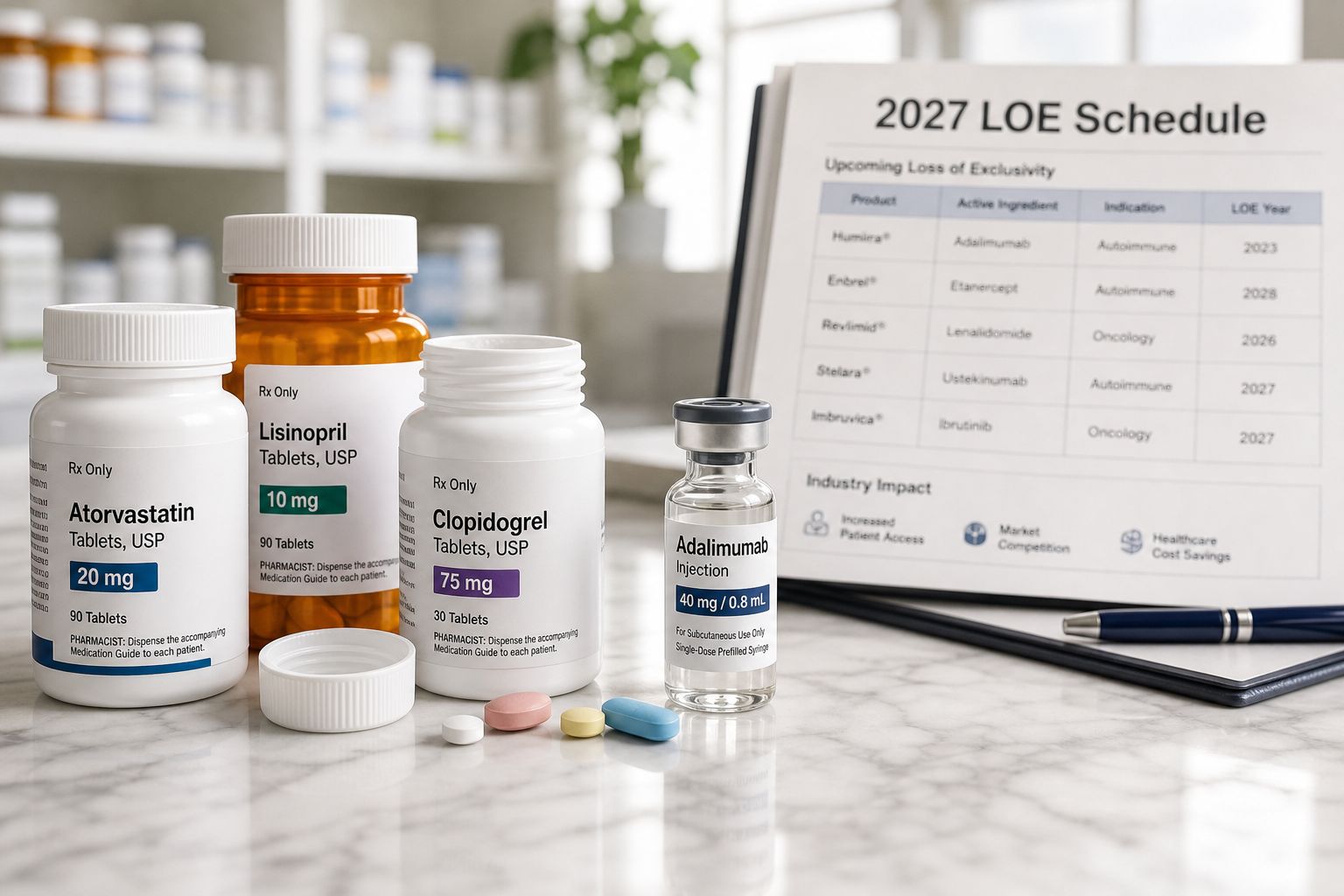

Market Challenges – Patent Expirations and Competition: A major challenge facing the industry is the “patent cliff,” wherein many blockbuster drugs lose market exclusivity over the next few years. Loss of exclusivity (LOE) allows lower-cost generic and biosimilar competitors to enter, eroding branded sales. From 2020 to 2025, the cumulative impact of LOEs is estimated at $170+ billion in lost brand sales globally, much of that due to biosimilar competition on biologic drugs ([1]). Key examples include the anti-TNF biologic Humira (adalimumab), which for years was the world’s top-selling medicine; Humira faced its first U.S. biosimilars in 2023 and has seen sales sharply decline (its worldwide revenue in the first half of 2025 dropped to ~$2.3 billion, a steep fall from prior years) due to multiple biosimilars capturing market share ([14]). Similarly, oncology biologics like bevacizumab (Avastin) and trastuzumab (Herceptin) lost exclusivity in recent years, with biosimilars driving prices down by 20–50% in many markets. IQVIA estimates that biosimilar competition will yield about $285 billion in cumulative savings globally from 2021–2025 as expensive biologics face lower-cost alternatives ([1]). This is a double-edged sword: on one hand, it constrains industry revenue growth in developed markets; on the other, it expands patient access to vital therapies (e.g., cheaper biosimilars for cancers or autoimmune diseases mean more patients can be treated within the same budget). The industry’s response to the patent cliff has been aggressive lifecycle management (developing improved formulations or new indications to extend a brand’s life) and pursuing next-generation products (e.g., AbbVie successfully replaced Humira’s revenue by promoting newer immunology drugs like Skyrizi and Rinvoq, which saw >60% growth in 2025 ([14])).

-

Market Challenges – Pricing and Access: Prescription drug pricing has become a flashpoint globally. Many advanced therapeutics launch with extraordinarily high prices – often hundreds of thousands of dollars for a year’s treatment (as seen with some cancer immunotherapies and rare disease drugs) – putting pressure on healthcare payers and patients. Health systems and governments worldwide are implementing measures to contain drug costs and ensure value for money. In the United States, which historically has had minimal price regulation, a significant development was the passage of the Inflation Reduction Act (IRA) of 2022, which for the first time empowers Medicare (the largest U.S. public insurer) to negotiate prices for certain high-cost drugs starting in 2026. This policy shift “shattered complacency” in pharma executives, prompting many companies to reassess revenue forecasts, R&D budgets, and pricing strategies for their portfolios ([15]). In Europe, most countries have long had strict price controls, reference pricing (benchmarking drug prices to other countries), and value assessment via health technology assessment (HTA) agencies. Payers in Europe continue to challenge high prices by, for example, refusing coverage for drugs deemed not cost-effective or negotiating confidential rebates. Even China has executed sweeping reforms to reduce drug prices – notably the Volume-Based Procurement (VBP) policy initiated in 2018, where the government conducts centralized bulk procurement tenders for drugs (mostly generics) in exchange for steep price cuts often exceeding 50%. This has slashed costs for many generic drugs in China’s hospitals, albeit at the expense of some multinational pharma revenues. Japan routinely cuts drug prices every two years to rein in spending. These converging global efforts underscore that pricing pressure is now a truly global phenomenon ([16]). Pharmaceutical companies are thus under intense scrutiny to demonstrate the value of their products – in terms of clinical benefit and health outcomes – to justify their costs. We see a rise in “value-based” pricing and reimbursement models, where payment for a drug may be conditional on patient outcomes (for instance, payers getting refunds or price adjustments if a drug doesn’t achieve expected results). Manufacturers are also offering patient support programs and outcomes-based contracts to appease payers and the public on cost concerns.

-

Public Health and Equity Considerations: Despite the industry’s growth and innovation, access to medicines remains uneven globally. There is a stark contrast between high-income and low-income regions. According to the World Health Organization, about 2 billion people (one-third of the global population) do not have regular access to essential medicines ([17]). In many low- and middle-income countries, life-saving drugs – even older generic medicines – are often unavailable or unaffordable for large segments of the population. For example, treatments for diseases like diabetes, cancer, or hepatitis that are standard in wealthier countries may be scarce in poorer nations. The COVID-19 pandemic threw this disparity into sharp relief: while wealthy nations rapidly purchased and administered new COVID vaccines in 2021, many low-income countries lagged far behind in vaccination rates due to supply and affordability issues. This has fueled calls for greater international support, such as vaccine donations, and for structural changes (like waiver of certain intellectual property rights in emergencies). The industry faces ethical and reputational pressure to address these gaps – through tiered pricing (selling drugs at lower cost in poorer markets), voluntary licensing to enable generic production, or partnerships with global health organizations. Some big pharma companies have launched initiatives to supply medicines at cost to developing countries for specific therapeutic areas, but significant challenges remain to achieve “medicines for all.”

-

Public Health Challenges – Antimicrobial Resistance (AMR): One notable area of concern is the shortage of new antibiotics. Antimicrobial resistance – where bacteria become resistant to existing antibiotics – is a mounting crisis that causes over 1.27 million deaths per year globally (as of 2019) ([18]). Yet, pharmaceutical R&D has largely shifted away from antibiotics because these drugs are less financially rewarding (they are used for short durations and priced low, and new antibiotics are often held in reserve to prevent resistance). Alarmingly, no truly new class of antibiotic has been developed in over 30 years ([18]). The antibiotic pipeline is described as “broken,” prompting governments and non-profits to intervene with new incentives (for example, the AMR Action Fund, a public-private partnership launched with a $1 billion investment to support biotech companies developing novel antibiotics ([19])). This issue illustrates the tension between public health needs and market forces: not all health priorities align with profit incentives, and thus some crucial areas require policy solutions to ensure innovation continues.

-

Impact of COVID-19 – Case Study: The COVID-19 pandemic (2020–2021) was a defining challenge for the pharmaceutical industry and, in many ways, a validation of its value to society. The industry responded with unprecedented speed to develop vaccines and therapeutics. In less than a year, multiple effective vaccines were developed, tested, and authorized – a process that normally takes a decade. mRNA vaccine technology (from Pfizer-BioNTech and Moderna) proved its worth, and viral vector vaccines (AstraZeneca-Oxford, J&J) and protein-based vaccines (Novavax) also contributed. By the end of 2021, billions of vaccine doses were produced, and a global vaccination campaign was underway. Pharma companies collaborated across borders and with governments (e.g., Pfizer partnered with the German biotech BioNTech; AstraZeneca with Oxford University; Merck & Co. teamed with smaller firms on antiviral research). Notably, public funding (such as the U.S. Operation Warp Speed) and advance purchase commitments de-risked much of the development. The outcome was not only billions in revenue for some companies – Pfizer’s COVID-19 vaccine (Comirnaty) and Moderna’s Spikevax together generated tens of billions of dollars in 2021–2022 – but also a demonstration of new platforms (mRNA technology) that are now being applied to other diseases like cancer and influenza. However, the pandemic also spotlighted disparities: high-income countries received the majority of early vaccine doses, and only by late 2021 did substantial quantities reach lower-income nations. The experience has sparked discussions about pandemic preparedness and how to ensure more equitable access to countermeasures in the future. For pharmaceutical R&D, COVID-19 accelerated innovation in areas such as mRNA, antibody therapies, and antiviral drugs (Merck’s molnupiravir and Pfizer’s Paxlovid were oral antivirals developed in record time). It also normalized faster regulatory processes (emergency use authorizations) and novel trial designs. In retrospect, COVID-19 proved the agility of pharma when backed by global focus and resources, and it left lasting legacies: mRNA vaccines are now being researched for HIV, Zika, and cancer; governments are more deeply engaged in vaccine manufacturing capacity; and the public gained a more nuanced view of pharma, seeing both lifesaving innovation and debates over intellectual property (e.g., calls for patent waivers on COVID vaccines).

-

Technological and Digital Transformation: The coming years will further be shaped by technology both in R&D and in patient care. Artificial intelligence (AI) and machine learning are increasingly deployed in drug discovery (for instance, to identify new drug candidates or optimize trial designs). Startups and big pharma alike are using AI-driven algorithms to sift through vast chemical libraries or genomic data to find promising molecules faster and more cheaply than traditional laboratory screening. While still early, there have been successes – e.g., the first AI-discovered drug candidates entering clinical trials for fibrosis and other diseases – and this could potentially shorten development timelines. Precision medicine also continues to expand, leveraging genetic diagnostics to tailor treatments to patients most likely to benefit (for example, identifying specific mutations in tumors to choose targeted cancer therapies). On the manufacturing and supply chain side, the industry is adopting advanced technologies like continuous manufacturing, automation, and blockchain for supply chain security. The pandemic highlighted supply chain vulnerabilities (e.g., reliance on certain countries for active ingredients); now companies and governments are exploring more resilient, digital supply networks for critical medicines ([20]). Additionally, pharmaceuticals are increasingly delivered with digital health tools – such as smartphone apps for patient monitoring, digital companion programs to improve adherence, and telemedicine for remote prescription management – especially in the wake of COVID-19’s telehealth boom. Biopharma companies see providing “beyond the pill” services (patient support programs, disease management apps, etc.) as a way to differentiate their products and demonstrate better outcomes, which can support their value propositions to payers ([20]).

In sum, the global pharmaceutical market in 2025 is a $1.6 trillion industry characterized by high innovation, shifting market dynamics, and multi-faceted challenges. It operates at the intersection of advanced science, public health needs, and economic pressures. The industry’s trajectory remains upward – analysts predict that by 2028–2030, global pharma revenues will likely exceed $1.8–2 trillion ([13]) and could approach $3 trillion by the mid-2030s if current trends continue ([21]). This growth will be propelled by continued scientific breakthroughs (in areas like cell/gene therapy, oncology, neurological disorders, and vaccines for emerging viruses) and by rising healthcare investment in developing regions. However, to sustain its success, the industry must navigate critical headwinds: pricing and reimbursement hurdles, the wave of patent expiries, regulatory reforms, and societal expectations for greater access and affordability. Companies are responding by evolving their business models – focusing on developing truly differentiated, value-adding therapies; optimizing their portfolios and R&D productivity (often via collaborations and acquisitions); and engaging with healthcare stakeholders to devise new pricing models that better align cost with outcomes. The pharmaceutical sector at this crossroads is poised for further expansion but also transformation, as it aims to deliver the next generation of cures and treatments in a way that is both medically impactful and economically sustainable worldwide.

(The following report provides an in-depth analysis of the world pharmaceutical market as of 2025, examining its historical evolution, current composition, and future outlook. It covers regional markets, therapeutic area trends, R&D and innovation patterns, leading companies and competitive strategies, as well as challenges around pricing, access, and regulation. Case studies and real-world examples are included to illustrate key points, and all data and factual claims are supported by citations to reputable sources.)

Introduction

Background and Significance of the Pharmaceutical Industry

Medicines have transformed human health over the past century. From the mass production of penicillin in the 1940s to the latest gene therapies, the pharmaceutical industry has been at the forefront of translating scientific discovery into tangible health improvements. The industry’s core purpose is the research, development, manufacture, and distribution of drugs that prevent or treat diseases. Its contributions are evident in extended life expectancies and improved quality of life globally – for instance, vaccines eradicated smallpox and sharply reduced polio; antiretroviral drugs turned HIV from a death sentence into a manageable chronic condition; cardiovascular drugs and cancer therapies have saved or prolonged millions of lives.

Economically, the pharmaceutical sector is a major component of the global economy and a key segment of healthcare expenditures. In many advanced countries, pharmaceutical spending accounts for 10–20% of total healthcare spending (with the rest on hospitals, clinics, etc.), underscoring medicines’ central role in modern healthcare delivery. The global pharmaceutical market has expanded vastly in recent decades, reflecting both population and economic growth, as well as an expanding array of treatable conditions. In 2001, worldwide pharma sales were on the order of a few hundred billion dollars; by 2014, sales topped $1 trillion for the first time ([13]) – a milestone illustrating the industry’s explosive growth in the early 21st century. This growth continued such that by 2022, global pharma revenues reached $1.48 trillion ([13]), and as of 2023–2024 the industry is roughly a $1.6–1.7 trillion market annually. Few industries have such a direct impact on human lives or command such levels of investment.

Pharmaceutical innovation tends to be high-risk, high-reward. Developing a new medicine is an expensive and lengthy endeavor: on average, it takes 10–15 years from the initial discovery of a potential drug molecule to bring it through laboratory research, animal studies, clinical trials, and regulatory approval ([22]). The process is also costly – recent analyses (including a widely cited study by the Tufts Center for the Study of Drug Development) have estimated the average R&D cost to develop one new approved drug at $2–3 billion USD (when accounting for the cost of failures and capital costs) ([22]). Moreover, for every drug that succeeds, many others fail somewhere in development. Despite these challenges, the industry has managed to sustain a robust pipeline of new treatments, funded largely by the substantial revenues from existing products. Major pharmaceutical companies typically reinvest 15–25% of their revenue into R&D ([23]), a reflection of the innovation-driven nature of this business.

The year 2025 finds the pharmaceutical industry at a pivotal moment. It stands astride the $1.6 trillion mark, having demonstrated remarkable resilience through the COVID-19 pandemic, and it is experiencing rapid scientific advancement in many domains (immunotherapy, genetic medicine, etc.). However, it also faces intensifying external pressures: greater scrutiny on drug prices, a more complex global regulatory environment, and expectations to address unmet medical needs from Alzheimer’s disease to antibiotic-resistant infections. The industry’s business model – historically reliant on a few blockbuster drugs marketed broadly – is evolving towards more targeted therapies and diversified portfolios, often in partnership with biotech innovators.

This report aims to present a comprehensive analysis of the world pharmaceutical market in 2025, examining how we arrived at this point and where we are headed. The analysis is structured into multiple sections covering the industry from different angles:

- The Historical Growth and Current Market Landscape section reviews how global pharma sales have grown over time and outlines the present market size, segmentation, and growth rates. This includes identifying the key contributors to the $1.6T market value and the differential growth patterns across regions.

- The Regional Market Perspectives section delves into major geographic markets – North America, Europe, Asia-Pacific (with emphasis on China and India), Latin America, and others – highlighting regional market sizes, growth drivers, and unique factors (e.g., U.S. pricing environment vs. European single-payer dynamics, etc.).

- The Therapeutic Area Analysis section ranks and discusses major therapeutic categories by sales, such as oncology, immunology, cardiovascular, metabolic diseases, neurologic disorders, infectious diseases, etc. It identifies which areas are growing fastest and why, citing examples of key drug classes and recent launches.

- The Innovation and R&D Trends section examines the state of pharmaceutical research: the pace of new drug approvals, the focus on specialty drugs and rare diseases, the integration of new technologies like AI, and the evolving role of biotechnology companies. It also addresses R&D productivity challenges and how companies are adapting to deliver innovative medicines more efficiently.

- The Competitive Landscape and Key Players section profiles the industry structure. This includes an overview of the major companies (their market shares, top products, and strategies) and the competitive dynamics including mergers and acquisitions, the rise of emerging-market pharma companies, and the interplay between Big Pharma and smaller biotech startups.

- The Economic and Policy Environment section discusses issues of drug pricing, patent expirations, and health policy changes affecting the industry. This encompasses topics like generic and biosimilar competition, pricing reform legislation, and global trade/IP considerations (for instance, the debates around patent rights vs. public health in contexts like pandemics or developing country access).

- The Case Studies and Examples are interspersed to illustrate broader points with concrete instances – such as the industry’s response to COVID-19, a case of a high-profile drug losing patent protection (and the aftermath in the market), and the growth of China’s domestic pharmaceutical sector as a case study in an emerging market shift.

- The Future Outlook section (implications and future directions) synthesizes the analysis to project where the pharmaceutical industry is heading over the next 5–10 years. It considers expected market growth (e.g., reaching $2T and beyond), scientific frontiers (like precision oncology, gene editing, etc.), potential disruptions (like breakthrough cures or digital therapeutics), and the ongoing challenge of balancing innovation with affordability and access.

Throughout this report, a professional, evidence-based tone is maintained, with extensive data and citations provided to support each point. The goal is to present a deep, multifaceted understanding of the global pharmaceutical industry’s status and trends. By covering multiple perspectives – scientific, economic, and societal – the report aims to inform stakeholders ranging from healthcare professionals and policy-makers to industry executives and academics. This holistic scrutiny is especially important because the pharmaceutical domain does not operate in isolation: it is intimately connected to public health outcomes, government policies, and societal expectations.

In summary, as of 2025 the world pharmaceutical market stands as a thriving but challenged ecosystem. It is flush with scientific opportunities — from curing rare genetic disorders to harnessing AI for drug design — but also under pressure to prove its value and equitably distribute its advances. Understanding the detailed dynamics of this industry is crucial, as decisions made within pharma (whether to pursue a certain drug target, how to price a new therapy, where to invest in manufacturing) have far-reaching impacts on global health and economics. The following sections will unpack these dynamics in detail, offering a granular look at the $1.6T global pharmaceutical industry and painting a picture of its current state and future trajectory.

Global Market Overview: Size, Growth, and Key Drivers

In this section, we provide a panoramic quantitative overview of the global pharmaceutical market, focusing on the current size (circa 2025), historical growth patterns, and the major factors driving expansion. We will examine total market value, growth rates, and segmentation by product type (prescription vs over-the-counter, small molecule vs biologic, etc.) to set the stage for deeper analysis in subsequent sections.

Historic Growth Trajectory

The pharmaceutical industry’s growth over the past few decades has been marked by both consistency and periods of acceleration tied to waves of innovation or major healthcare expansions. To appreciate the 2025 market context, it is instructive to look at how the global pharma market reached its current scale:

- Early 2000s: In the year 2000, the global pharmaceutical market was valued around $390 billion (roughly estimate based on historical data and reports) – this was an era dominated by breakthrough small-molecule drugs for common conditions (statins for cholesterol, SSRIs for depression, ACE inhibitors for hypertension, etc.). The growth in the late 1990s and early 2000s was robust, often high single-digit percentage annually, fueled by large Western markets and the launch of blockbuster drugs targeting mass diseases.

- Mid-2000s: By 2005–2006, global sales had passed the half-trillion dollar mark. A PricewaterhouseCoopers report in 2007 noted the market was about $600 billion in 2007 and projected it could double to $1.3 trillion by 2020 ([24]). This was a time when emerging markets started contributing more significantly (the PwC report coined the term “E7” for seven emerging countries that could rise to 20% of global sales by 2020 ([25]), which indeed came to fruition). However, growth was somewhat tempered in late 2000s by patent cliffs of some 1990s blockbusters and the global financial crisis of 2008–2009 (which affected healthcare spending in some markets).

- 2010s – Crossing $1 Trillion: In 2014, as noted, the pharmaceutical market revenue crossed $1 trillion for the first time ([13]). Key growth drivers in the early-to-mid 2010s included the advent of novel hepatitis C cures (Sovaldi and its successors launched in 2013–2014, which had enormous sales albeit short-lived due to curing patients), the continued strength of biologics in autoimmune diseases and cancer, and the expansion of access (for instance, the Affordable Care Act in the U.S. expanded insurance coverage to millions, boosting drug utilization). During 2010–2015, global growth rates were typically in the 5–8% range annually ([26]), although dynamics varied by region – emerging markets often saw double-digit growth, while mature markets had slower expansion due to cost pressures. By 2017, worldwide pharma sales were roughly in the $1.2 trillion range.

- Late 2010s: Heading into 2020, the market was fast approaching $1.4 trillion. Indeed, one estimate pegged the market at $1.43 trillion in 2020 ([22]) as anticipated by earlier projections. This period saw the rise of immuno-oncology (notably checkpoint inhibitor drugs like Keytruda and Opdivo) which created multibillion-dollar markets almost from scratch, and orphan drugs becoming a major segment. Also, several large acquisitions consolidated some players (e.g., the 2019 BMS-Celgene and AbbVie-Allergan deals). Toward 2019–2020, growth slowed marginally in some markets due to large drugs losing patent (e.g., biosimilars for Rituxan, Herceptin, etc., hitting Europe around 2018 and the U.S. by 2019–20).

- 2020–2021 (Pandemic Impact): The advent of COVID-19 in early 2020 was a shock to the global economy and healthcare systems. Surprisingly, the pharmaceutical market proved resilient and even critical in this period. While non-COVID healthcare usage initially dropped (e.g., fewer doctor visits and elective prescriptions in lockdowns), the massive demand for COVID-19 vaccines and therapeutics in 2021–2022 more than offset those dips. Pharma revenues in 2021 surged notably due to tens of billions in vaccine sales. For example, Pfizer’s total revenue in 2021 jumped by ~95% (to $81 billion) largely due to its COVID-19 vaccine, and Moderna saw its first major commercial revenue (~$18 billion in 2021 from zero in 2019) due to its vaccine. Global pharmaceutical sales in 2021 likely exceeded $1.4 trillion and in 2022 reached about $1.48 trillion ([13]). COVID products became the top-selling pharmaceuticals globally in 2021–2022 – for instance, Pfizer/BioNTech’s Comirnaty vaccine topped ~$37 billion in 2021 sales, higher than any drug in history for a single year, and remained very high in 2022 (though these revenues are expected to fall sharply by 2023–2024 as the acute phase of the pandemic wanes).

- 2023 and onward: By 2023, with COVID vaccine revenues declining (as initial vaccination campaigns concluded and moved to smaller booster markets), the pharmaceutical market normalized to some extent. Still, 2023’s global market is estimated around $1.6 trillion ([27]). Growth continues to be driven by new product launches and the expansion of therapy use in emerging markets, while tempered by patent losses and cost controls.

Table: Global Pharmaceutical Market Value Over Time

To summarize the historical growth, the following table highlights global pharmaceutical market size at key milestone years, illustrating the trajectory toward 2025:

| Year | Global Pharma Market Revenue | Notes |

|---|---|---|

| 2000 | ~$390 billion | (approximate; start of century baseline) |

| 2005 | ~$600 billion | Rapid growth, driven by blockbusters & expansion |

| 2010 | ~$950 billion | Approaching $1T, boosted by biologics & emerging markets |

| 2014 | $1.05 trillion | First time exceeding $1 trillion [Statista] |

| 2017 | ~$1.2 trillion | High new drug output (Hep C cures, IO drugs) |

| 2020 | $1.42 trillion | Despite pandemic onset; strong innovation [PwC/Statista] |

| 2022 | $1.48 trillion | Peak of COVID vaccine impact [InvestingNews/Statista] |

| 2023 | $1.60 trillion (est.) | Normalizing post-COVID, robust growth in specialties [Statista] |

| 2025 | $1.6+ trillion (proj.) | Projected continued growth to ~$1.6T (excl. COVID vax) [IQVIA] |

Sources: Compiled from Statista, PwC, IQVIA Institute and industry reports ([13]) ([5]) for global market estimates.

As shown, the pharma market roughly quadrupled from 2000 to 2020 (from ~$390B to $1.4T) and has since added further growth. Even adjusting for inflation, this represents massive real expansion. Key inflection points have been in the mid-2000s (when emerging markets started surging), early 2010s (first trillion-dollar year), and early 2020s (COVID bump). By 2025, we see a stabilization around the $1.6 trillion level, which will serve as the baseline for further growth toward 2030.

Current Market Size (2025) and Composition

Going into 2025, global pharmaceutical spending is about $1.6 trillion annually. IQVIA’s widely cited projection put it at $1.6 trillion by 2025 using invoice price levels (ex-COVID vaccines) ([1]). This figure encompasses all medicinal products: branded prescription drugs, generic drugs, biologics, and often over-the-counter (OTC) medicines as well (depending on the definition – IQVIA typically refers to the “medicine market” including prescriptions; Statista’s $1.7T for 2024 included both prescription and nonprescription).

It’s important to delineate what contributes to this $1.6T market:

- Prescription Drugs: The majority of the market value (~80% or more) comes from prescription medications (those that require a physician prescription, including brand-name drugs and their generic equivalents, as well as biologics and biosimilars). Within prescription drugs, one can further distinguish branded (on-patent) drugs versus generic drugs. Branded drugs command higher prices and thus a disproportionately high share of revenue relative to volume. Generic drugs (small-molecule off-patent drugs produced by multiple competitors) tend to be low-priced and high-volume. For instance, generics account for an estimated 70–80% of prescription volume in many markets by 2025, but far less in value (in the U.S., generics are ~90% of prescriptions but only ~20% of drug spending due to their low prices).

- Biologic vs Small Molecule: A significant shift in composition is the rise of biologic therapies (large, complex protein-based drugs, usually injectable) relative to traditional small-molecule drugs (chemically synthesized pills, capsules, etc.). Biologics often come at premium prices and treat complex conditions (cancers, autoimmune diseases, etc.), thus capturing a large share of spending. By mid-2020s, biologics make up an estimated 35–40% of the pharma market by value and this share is climbing (projected to exceed 50% by 2030 as mentioned) ([6]). Many of the top-selling products globally – such as monoclonal antibodies like Keytruda (oncology), Opdivo (oncology), Humira (immunology), and Enbrel (immunology), or insulin analogs for diabetes – are biologics.

- Specialty vs Primary Care: The industry often categorizes drugs into “specialty” vs “primary care” (or traditional). Specialty drugs typically require special handling, administration, or monitoring, and are frequently high-cost drugs used in serious conditions (e.g., biologics for rheumatoid arthritis, oral targeted cancer drugs, etc.). We noted earlier that specialty drugs are about half of all spending by 2025 ([5]). The remaining share is more primary care drugs – think of common oral medications for blood pressure, cholesterol, diabetes (though newer diabetes drugs like GLP-1s are becoming specialty-level expensive), antidepressants, antibiotics, etc., many of which are available as generics.

- Over-the-Counter (OTC) Medicines: Non-prescription pharmaceuticals (like pain relievers, cough and cold remedies, supplements, etc.) are also a multi-billion dollar market segment globally. Statista estimated OTC drug sales worldwide to be on the order of ~$140 billion in 2020 and growing towards $200 billion by late 2020s ([28]). While significant, OTC is much smaller than the prescription market and typically not included in all “pharma market” definitions. In this report, unless otherwise specified, figures like the $1.6T primarily refer to prescription medicines.

Thus, the $1.6T market in 2025 is predominantly driven by prescription, innovative (often specialty) pharmaceuticals. A breakdown by therapeutic categories (which we will detail in a later section) would show largest contributions from oncology, immunology, diabetes, cardiovascular, etc. For context, by 2025 oncology alone represents roughly 17% of global spending (given $273B out of $1.6T) and immunology ~11%. Traditional primary care areas like cardiovascular (including lipid-lowering drugs, antihypertensives) have a big volume but many generic products, so their share of spending has declined over time (as key drugs like statins, older antihypertensives went generic). Infectious disease drug spending is somewhat bifurcated: the routine anti-infectives (antibiotics) are mostly generic and cheap (small share of spend), whereas vaccines and some antivirals can be lucrative (e.g., the Pfizer and Merck COVID antivirals, HIV antivirals, etc.).

Another lens is the geographic composition of that $1.6T. We will cover regional specifics later, but at a high level: North America (especially the U.S.) likely comprises over half of the $1.6T spending in 2025, while Europe accounts for roughly 20%, Asia-Pacific (including China, Japan, India, etc.) around 20–25%, and the rest of world (Latin America, Middle East, Africa, etc.) the remainder. The U.S. in particular, with around $600–700 billion in medicine spending by mid-2020s, is singularly large ([3]). China’s market, by comparison, is on the order of $170–200 billion in 2025 (depending on sources) ([3]), and Japan’s around $80–90 billion. Aggregating the so-called “pharmerging” countries (a set defined by IQVIA that often includes ~21 high-growth developing markets including China, Brazil, India, Russia, Turkey, Mexico, etc.), their share has been rising. In 2007, emerging markets might have been ~20% of global pharma; by 2023 they are likely around one-third of global spending. This shift reflects both the economic growth enabling higher healthcare spending in those countries and deliberate policy efforts to expand access to medicines for their populations.

Growth Drivers in 2025

Understanding what fuels market growth in 2025 is crucial for context. The major growth drivers can be categorized into demographic/epidemiologic factors, innovation/clinical factors, and economic/policy factors:

-

Demographics & Epidemiology: The world’s population is growing and aging. Particularly, the proportion of people over 60 is rising rapidly in many regions (especially in developed countries and in places like China). Older populations have higher prevalence of chronic diseases (like cardiovascular disease, arthritis, cancer), leading to greater medication use. For instance, the global prevalence of diabetes and cancer have been increasing, driving demand for anti-diabetic drugs and oncology therapies. Moreover, the lifestyle and epidemiological transition in developing countries means they are now grappling with both infectious diseases and the same chronic diseases seen in rich countries (due to urbanization, dietary changes, etc.). For example, emerging markets have seen spikes in hypertension, diabetes, and cancer rates as their economies grow, which increases the need for modern medicines ([24]). Thus disease prevalence is a fundamental driver: more patients = more medication use, all else equal.

-

Advances in Medical Science and New Product Launches: The constant flow of new and improved therapies is perhaps the strongest propellant of market growth. When a novel drug addressing an unmet need comes out, it can create a new revenue stream where none existed or replace older less effective treatments at a higher price point. In recent years, breakthroughs in molecular biology, genomics, and immunology have yielded first-in-class drugs for diseases that previously had limited options (e.g., checkpoint inhibitors that unleash the immune system on cancers, disease-modifying therapies for rare genetic disorders, etc.). Each year, dozens of new drugs (including high-price specialty drugs) enter the market – e.g., gene therapies for spinal muscular atrophy and other inherited diseases, new oral therapies for cystic fibrosis, etc. Each such launch contributes incrementally to market growth. The period up to 2025 has some highly anticipated launches: for instance, new weight-loss drugs (like Lilly’s tirzepatide in obesity, recently approved as Zepbound, following the success of semaglutide) will significantly expand the metabolic category; new Alzheimer’s disease drugs (e.g., lecanemab, trade name Leqembi, approved 2023, and others in pipeline) could create a large new therapy area if broadly adopted; there are also cutting-edge cell therapies and gene therapies coming for cancer and blood disorders. Evaluate Pharma’s preview for 2025 highlighted that over 70 novel drug approvals are expected in 2025 alone, which together could add >$80 billion in new sales that year ([7]). In short, innovation is the lifeblood of the pharma market’s growth – each successful new drug can command significant revenue, especially if it addresses a critical illness or has superior efficacy.

-

Expanding Healthcare Access & Expenditure: In many parts of the world, both government and private healthcare spending are on the rise. Countries are investing more in healthcare infrastructure and insurance coverage. For example, China in the past 15 years rolled out broad public insurance and improved its Essential Drug List coverage, enabling many more patients to use reimbursed medicines. India has in recent years launched schemes for wider health coverage (e.g., Ayushman Bharat). Across emerging markets, the aspiration to improve healthcare outcomes translates into higher pharmaceutical consumption as more patients get diagnosed and treated for conditions. Even in developed markets, initiatives like preventive healthcare and early detection (e.g., more aggressive treatment of high cholesterol or pre-diabetes) can increase medicine usage. According to SNS Insider, rising healthcare expenditure worldwide, along with efforts to enhance healthcare access, is a key factor propelling pharmaceutical market growth ([21]). An aging population not only has more disease but also typically leads governments to spend more (e.g., on subsidized prescriptions for the elderly via Medicare in the U.S. or similar programs elsewhere).

-

Economic Growth in Emerging Markets: Closely tied to access, the rapid economic development in countries like China, India, Brazil, and others has made medicines more affordable at both the personal and national level. A larger middle class means more people can pay out-of-pocket for medications or afford private insurance. Government health budgets also grow with GDP. China’s pharmaceutical market, for instance, grew exponentially from about $20 billion in 2000 to over $150 billion by 2020, tracking its economic expansion. Emerging markets often have higher volume growth, as basic healthcare needs are met for previously underserved populations. This volume growth can counterbalance price lowering measures (like China’s VBP). The net effect is strong growth in absolute sales.

-

Product Mix Shift to Higher-Value Medicines: Even without more patients, the market can grow if patients shift to newer, more expensive therapies that provide better outcomes. This treatment intensification is evident in many fields: e.g., diabetic patients moving from inexpensive older oral pills to newer GLP-1 injectables that cost orders of magnitude more, or cancer patients moving from generic chemotherapies to targeted therapies/immunotherapies that can cost tens of thousands of dollars per month. As the standard of care elevates globally to include advanced therapies, the average spending per patient for many conditions increases accordingly. The IQVIA report noted that adoption of new treatments in developed countries and increased use of new medicines in pharmerging markets are significant drivers of spending growth ([5]).

-

Pandemic Aftermath and Health Priorities: The COVID-19 pandemic left some indirect impacts that may bolster pharma markets in the mid-2020s: governments became more cognizant of infectious disease threats and may stockpile certain drugs or vaccines, ongoing COVID-related spending (boosters, antivirals) adds a modest but present stream, and public awareness of vaccines and medicines increased. Additionally, the pandemic caused some patients to delay treatments in 2020–21, which could result in higher utilization later as they catch up on care. However, the pandemic also strained budgets, so this is a nuanced factor.

Collectively, these drivers set up a scenario where even as mature markets face headwinds (patent cliffs, pricing pushback), global pharmaceutical spending can continue to climb, fueled particularly by emerging market uptake and scientific progress unlocking new markets.

Current Growth Rate and Near-Term Forecast (2025)

As of 2025, global pharmaceutical spending growth is in a moderate range. IQVIA projects a 3–6% CAGR from 2020 through 2025 ([1]), which is a solid, if not spectacular, growth rate compared to historical double digits but understandable given the large base and increasing influence of cost controls. The mid-point of that range would suggest roughly 5% annual growth. Indeed, excluding the one-time COVID bulges, the pharma market growth has settled in mid-single digits. Certain segments, however, are growing much faster – for example, oncology and immunology (high single or low double digits), whereas some segments like primary care small molecules in developed markets are flat or declining (due to generics).

Evaluate Pharma’s 2025 World Preview suggests prescription drug sales globally will grow at over 7% CAGR up to 2030 ([6]), indicating perhaps a slightly more optimistic outlook for medium-term growth (likely factoring in new high-value products offsetting patent losses). In absolute terms, this means adding tens of billions in new spending each year.

Looking just ahead, 2024 and 2025 themselves are expected to see re-accelerating growth as the industry “recovers” from the pandemic-era distortions. For instance, the large revenue drop in COVID vaccine sales from 2022 to 2023 created a headwind, but beyond that, underlying growth in non-COVID areas is strong. Evaluate’s analysis for 2025 noted the sector would be back in “recovery mode” from the pandemic trough, expecting substantial new sales from the obesity and oncology drug launches ([7]). Specifically, 2025 is anticipated to be a year of “rallies” in pharma with over $80 billion in additional sales from new products versus the previous year ([7]), which is quite significant (for comparison, $80B incremental is roughly +5% on a $1.6T base).

Beyond 2025, forecasts converge that growth will continue. For example, BCC Research projects the market to hit $2.2 trillion by 2029 ([29]) and Precedence Research forecasts over $3 trillion by 2034 ([30]), though such long-range forecasts are inherently uncertain. Nonetheless, the consensus is clear that the trajectory is upward, provided no catastrophic global event derails it. The growth may not be as explosive percentage-wise as in earlier eras (since the base is now huge), but in absolute value, the industry is poised to add hundreds of billions more in the coming decade.

To conclude this overview: the world pharmaceutical market in 2025 stands at roughly $1.6 trillion, having grown steadily through the last decades and showing resilience even through global upheavals. It is a market increasingly driven by innovative therapies, expanding global access, and shifting toward specialty care. The growth rate is moderate but steady, and longer-term prospects remain positive given the constant pipeline of new medical advances and the undiminished global demand for better health and longer lives. In the next sections, we’ll dissect this big picture into more detail by region and by therapeutic sector, and examine the complexities behind these aggregate numbers.

Regional Perspectives: Markets and Trends Across the Globe

While the pharmaceutical industry is often discussed in global terms, it is far from a monolithic market. Regional differences in epidemiology, economics, healthcare infrastructure, and policy lead to significant variability in how the pharma market operates and grows in different parts of the world. In this section, we break down the world pharmaceutical market by key regions and countries: North America (especially the U.S.), Europe, Asia-Pacific (with focus on China, India, Japan), Latin America, and other notable markets. We will highlight the size of each regional market, their growth rates, and unique drivers or challenges they face.

North America: The Dominant Market

North America, particularly the United States, is the largest and most lucrative region for pharmaceuticals. As of 2024, North America accounts for slightly over 50% of global pharmaceutical sales by value ([3]). This is striking considering the region has only about 5% of the world’s population; it reflects higher spending per capita on medicine due to wealth, high drug prices, and broad access.

-

United States: The U.S. alone was projected to spend $685–715 billion on medicines in 2026 ([3]), implying around $600+ billion in 2025. Indeed, Statista reported U.S. prescription drug sales around $800 billion in 2024 (though this number might include some double counting or different methodology, it underscores the scale) ([3]). The U.S. market is characterized by minimal price controls compared to other countries, meaning manufacturers often set high launch prices and can take price increases. Even though private insurers and pharmacy benefit managers negotiate some rebates, on the whole U.S. drug prices (especially for brand-name drugs) are significantly higher than in other countries, boosting revenue. The U.S. also tends to be the earliest adopter of new technologies – new drugs often get approved first by the FDA and are taken up quickly by physicians and patients, especially in certain segments like oncology or rare diseases where insurance will cover high-cost treatments. This “early and broad uptake” dynamic contributes to the U.S. being about 53% of the global prescription drug market by value ([3]) despite representing only ~20% of volume in some estimates. The U.S. market has grown steadily, boosted in the 2010s by Medicare Part D (government drug insurance for seniors introduced in 2006) and by population aging. However, as of 2025, the U.S. growth is modest in net price terms – IQVIA projected the U.S. net medicine spending CAGR at 0–3% for 2020–2025 ([1]), indicating that while gross sales rise with new products, factors like patent expiries and rebate pressures keep net growth low. Notably, the U.S. is about to face a wave of high-profile LOEs (e.g., Eylea in 2024, Enbrel in 2029, Keytruda in 2028, etc.) which temper projections. Another key development: the Inflation Reduction Act (IRA). Starting 2026, Medicare will negotiate prices for a small selection of top-selling older drugs ([31]), and also impose penalties on price hikes above inflation. While the immediate effect will hit after 2025, it casts a long shadow as pharma companies in 2025 are already strategizing pipelines and pricing assuming a more constrained U.S. pricing environment. According to industry analysts, the IRA’s provisions (along with existing payer pressures) will likely slow U.S. market growth beyond mid-decade ([15]). Despite these challenges, the U.S. will remain the primary market that pharma companies target for returns, given its sheer size and historically favorable margins. Another feature: the U.S. is a major hub of pharmaceutical R&D and biotech investment, creating a virtuous cycle where breakthroughs often originate or are first commercialized in the U.S.

-

Canada: Canada’s pharmaceutical market, though much smaller (~$30 billion in 2022 sales, roughly 2% of global), is a stable, developed market. It has a single-payer health system in each province which negotiates drug prices nationally (through the Patented Medicine Prices Review Board and the pan-Canadian Pharmaceutical Alliance). Canadian drug prices are generally lower than U.S. but higher than European averages. The market mostly mirrors trends of other advanced countries – high use of generics (Canada has over 70% of prescriptions dispensed as generics), growing use of specialty drugs, etc. One ongoing debate in Canada is the potential introduction of national pharmacare (universal drug coverage) which could expand access to medicines for uninsured populations, but also might impose stricter pricing. Regardless, Canada’s growth is moderate, reliant on introduction of new therapies as the population growth is slow.

North America as a whole is expected to continue growing in absolute terms but its share of the global market might slightly shrink over time as other regions grow faster. In 2010 North America was under 50%; by 2024 it’s just over 50%. Evaluate forecast that North America’s share might hold around ~50% at least through the decade, meaning it grows roughly in line with global average.

Europe: A Diverse but Mature Market

Europe collectively is the second-largest pharmaceutical market, but it is fragmented into many national systems. The European Union (EU) plus the UK (often analyzed together) makes up roughly 20–25% of world pharmaceutical sales. For example, the five biggest EU markets (Germany, France, Italy, Spain) plus the UK and some others contribute significantly. Statista indicates the top 5 country markets after the US and China include Japan (~7%), Germany (~5%), France (~3%), etc., with combined Europe around ~15% for top five and more with rest ([3]). However, note those shares might be for prescription market only.

Key characteristics of Europe’s pharma market:

-

Market Size and Growth: Europe’s pharma market (EU27 + UK) was valued around $300–350 billion in the early 2020s. Growth in Europe is relatively low (a few percentage points annually) due to heavy cost containment policies. IQVIA forecast Europe (defined as EU and some non-EU Europe likely) to grow about 2–5% CAGR to 2025 adding only around $35 billion in spending ([1]). This is markedly lower than emerging market growth and slightly below U.S. growth. The slow growth is primarily because most European governments aggressively negotiate drug prices and have mechanisms to limit budget impact (such as caps, payback schemes where companies reimburse gov’t if spending exceeds certain growth, etc.). Also, Europe had an earlier exposure to biosimilars than the U.S. (biosimilars for key biologics launched in EU around 2015–2018, years before U.S.), translating to significant savings and reduced growth in those segments.

-

Pricing and Access: Europe is known for its reference pricing and HTA (health technology assessment) processes. Countries like Germany initially allow free pricing for a new drug but then assess its added benefit via the IQWiG/G-BA process within a year to decide price negotiations (early indications show, for example, that if no added benefit is proven, German insurers will only pay a price comparable to existing therapies). France has a system of ASMR rating that influences price. UK (through NICE) conducts cost-effectiveness analysis (quality-adjusted life year cost) to decide if the National Health Service will cover a drug, often demanding price discounts to meet thresholds. These processes mean that some drugs are launched later or at lower prices in Europe compared to the U.S.. On average, new medicines reach European patients 6–12 months after U.S. launch, sometimes more, and often at 20–40% lower list price (or even greater differences after U.S. rebates considered) ([32]). Europe’s unified stance on pricing (with cross-country collaborations to share pricing information or jointly negotiate, as seen with the Beneluxa initiative or EU joint procurement for some drugs) is strengthening. This environment restrains market growth but ensures wider population coverage in those countries.

-

Regional Variation: Within Europe, Western European countries (Germany, France, UK, Italy, Spain) are the largest markets. Germany is the single largest European drug market (roughly €50 billion+ in 2022 pharmaceutical sales), known for relatively quick uptake of new drugs (Germany often launches most new drugs first in Europe due to its initial free pricing period). France and Italy follow, each with strong domestic pharma industries as well (Sanofi from France, multiple companies in Italy). The UK is about a 3% global share market – smaller population but still significant in innovation (AstraZeneca, GSK are UK-rooted). Spain also significant. These five together often constitute ~70% of EU market value. Northern Europe (Sweden, Netherlands, etc.) and Southern/Eastern Europe have smaller markets; Eastern European countries spend much less per capita on medicines, though their growth rates can be higher as their economies converge.

-

Generic Usage: Europe widely uses generics and, increasingly, biosimilars. Countries like the UK and Germany have high generic penetration (the UK has over 80% of prescriptions dispensed as generics). Generic prices in Europe are typically much lower than in the U.S. – after patent expiry, European payers leverage competition and reference pricing to drive prices often to 20% or less of the brand cost within a few years. This yields savings but again reduces revenue for companies, contributing to slower growth. Biosimilar adoption in Europe has been very successful: for instance, after biosimilar introduction, the price of drugs like adalimumab (Humira) in some EU markets fell by 60–80% and biosimilar market shares exceeding 75% within a year or two. This is encouraged by policies (like automatic substitution in some countries, physician quotas, etc.).

-

Future Outlook in Europe: One development is the proposed EU Pharmaceutical Strategy and reforms (as of 2023–24, the European Commission is working on the biggest overhaul of pharma legislation in 20 years, aiming to speed up drug approvals, address drug shortages, and adjust incentives like reducing exclusivity for companies that don’t launch drugs in all EU countries quickly). Such policy changes could affect the market by possibly improving access speed (which might increase uptake) but also by shortening market exclusivity if conditions aren’t met. European payers are also increasingly exploring outcome-based agreements and managed entry agreements for ultra-expensive therapies (like gene therapies). For example, Italy’s system has for years had outcome-based payment where if a drug doesn’t work, the company might refund part of cost.

-

Europe’s Share & Growth: Europe’s share of global pharma might gradually decline just due to higher growth elsewhere. Evaluate’s preview data indicates that while the market grows, Europe’s relative piece shrinks a bit. The pharmerging vs developed dynamic is at play – in IQVIA’s terms, Europe plus U.S. etc. (developed markets) are slow, whereas emerging picks up more share. A Statista forecast predicted developed markets as a group will hold about 63% share by 2027, down from 69% in 2022, with emerging growing from 31% to 37% ([33]). Europe is a big chunk of that developed pie, so essentially its growth lags global average slightly.

In summary, Europe remains a critical region – it contributes a quarter of sales and is home to several top pharma companies (Roche, Novartis, Sanofi, GSK, AstraZeneca, etc.). Patients in Europe generally have high access to medicines albeit sometimes with delays, thanks to universal health systems. The market is mature: growth comes from therapeutic innovation because population growth is stagnating and budgets are tight. Europe’s approach emphasizes sustainability – trying to balance rewarding innovation with affordability – which often means lower prices, higher volume compared to the US’s high price/lower volume (some uninsured can’t access) model.

Asia-Pacific: Rapid Growth and Emerging Innovation

The Asia-Pacific (APAC) region is extremely heterogeneous, encompassing highly developed markets like Japan and Australia, huge emerging markets like China and India, and many smaller markets. As a whole, Asia-Pacific’s share of the pharma market has been rising, primarily because of China’s explosive growth and other emerging Asian economies. By 2025, APAC (including China, India, Japan, South Korea, Australia, ASEAN countries, etc.) likely accounts for roughly 30% of global pharmaceutical spending, up from perhaps ~20% a decade prior.

Let’s consider key players in APAC:

China: The Pharmerging Giant

China is the world’s second-largest pharmaceutical market as of 2025. The Chinese pharma market was estimated around $170–190 billion in 2021, and projected to grow to ~$200+ billion by 2025 ([3]) (some forecasts say $180–220B by mid-decade depending on data inclusion). However, measuring China’s market size can vary: some sources only count sales in certain channels (like hospital drug sales), and currency fluctuations matter. Nonetheless, China’s importance is undeniable.

Growth: China’s pharmaceutical spending growth was extremely high in the 2000s and 2010s (often >15% annually), making it leap from the 8th largest market in 2006 to 2nd largest by 2017. In recent years, growth moderated due to heavy price reforms (VBP tenders slicing generic prices, negotiation of blockbuster prices, etc.) but still remains in mid-to-high single digits in volume and a few percent in value. IQVIA noted China will accelerate post-COVID with greater uptake of new innovative medicines ([1]), especially as the government has been improving its drug approval and reimbursement processes.

Drivers in China:

- Healthcare Reform and Insurance: A major driver was China’s expansion of health insurance over the last decade. Now over 95% of the population has basic medical insurance ([34]). The government also added many drugs to the National Reimbursement Drug List (NRDL) in recent years, including a policy of annual negotiations to include new innovative drugs in coverage in exchange for huge price cuts. For example, PD-1 cancer immunotherapies from domestic firms, as well as global drugs like Merck’s Keytruda, saw >60% price cuts to get on NRDL, but then their volume and sales boomed due to broad reimbursement.

- Volume-based Procurement (VBP): Starting 2018, China implemented centralized tendering for generics (and now expanding to some off-patent original brands), where winners (often domestic generic companies) get exclusive large-volume contracts in hospitals if they offer very low prices. This dramatically reduced prices of common generics (e.g., statins, blood pressure meds, etc., many dropped by 50-90%). While this slashes margins for generic firms, it freed up budget space that China is using to pay for new innovative drugs. So, it’s a redistribution: the overall spending may grow slower, but more of it shifts to innovative drugs from expensive originators now available cheaper.

- Local Industry Growth: China historically was known for generics and APIs, but in the last 5-10 years it has poured investment into biopharmaceutical innovation. Dozens of local biotechs have sprung up (often funded through venture capital and government incentives), and they’ve produced innovative drugs especially in oncology. By 2025, China has approved several domestically-developed novel drugs (e.g., PD-1 inhibitors like Camrelizumab, CAR-T cell therapies for leukemia, etc.). Evaluate reported a remarkable stat: China-sourced innovative assets accounted for just 3% of global pharma licensing deals in 2020, but are expected to make up almost 40% by 2025 ([6]). This indicates Chinese biotechs are increasingly striking deals to have their drugs marketed globally by Western firms, reflecting the country’s rise as an innovation hub. The Chinese government’s support via regulatory reforms (like joining ICH, which harmonized standards, and speeding up approvals of new drugs) and funding have catalyzed this.

- Urbanization and Chronic Diseases: With economic development, Chinese patient demographics changed – there’s much higher incidence of cancers, heart disease, diabetes than a few decades ago, due to lifestyle changes and aging (China’s population is aging rapidly because of its size and one-child policy legacy). Treating these conditions is a priority, driving sales of both traditional drugs (e.g., insulin sales in China skyrocketed) and new targeted therapies.

Challenges in China: The aggressive cost-cutting measures mean that, ironically, the days of double-digit growth might not return; growth is now more in line with global average or slightly above. Also, regulatory policies can be a wild card – lately China signaled potential controls on drug profit margins and distribution reforms. Another challenge: intellectual property (IP) and quality concerns historically impacted perceptions, but China has improved IP protections and enforcement as it wants to foster innovation.

Outlook: Many analysts see China continuing to be a top growth contributor in absolute dollars. The Evaluate 2025 Preview emphasizes China’s rapid biopharma rise will fundamentally change the global industry ([6]). Chinese companies are expected to not only dominate their massive domestic market but increasingly compete internationally with novel products (for example, in 2021, China's BeiGene got its homegrown BTK inhibitor Brukinsa approved by the FDA, showing Chinese drugs going global). So by 2025, China is not just an end market, but also an emerging source of competition and innovation.

Japan: A Mature Market in Transition

Japan has historically been the second-largest single country pharma market (until China surpassed it around mid-2010s). Japan’s market is notable for its high per-capita drug spend and a traditionally innovation-friendly environment (Japan often had quick uptake of new drugs and higher prices, especially pre-2000s). As of early 2020s, Japan’s pharmaceutical market size is around $85–95 billion per year. Its growth has been flat to negative in recent years when measured in yen (due to government price cuts, a stagnating economy, and a push for generics).

Key factors for Japan:

- Biennial Price Cuts: Japan’s national health insurance system sets drug prices in a fee schedule and historically cut them every two years. More recently, for drugs with huge sales or if market prices fall, they even instituted annual cuts. The government’s goal is to reduce healthcare costs as the population ages (Japan has one of the oldest populations in the world). As IQVIA noted, Japan will have flat-to-declining spending through 2025 because of continued price cuts ([1]). Despite introduction of new therapies, the systemic price revisions erode growth.

- Generic Promotion: Traditionally, Japan had low generic usage (culturally many physicians and patients preferred brand names). But that changed with policy – the government set targets to raise generic volume share to >80%. By 2020, Japan achieved around 80% generic penetration in volumes for drugs whose patents expired ([35]) – a big shift. This has saved costs but again reduced revenue for off-patent brand drugs that lingered on higher prices before.

- Innovative Drug Uptake: On the positive side, Japan rewards true innovation by granting premiums for new drugs (if a drug is classified as breakthrough or significant improvement). Japan also has an early access pathway and tries to accelerate approvals (the drug lag between Japan and US/EU has shortened greatly in the past decade). Japanese patients now often get new cancer drugs or rare disease therapies fairly soon after global approval. This keeps Japan an important launch market, albeit companies know the price will be cut at the next cycle.

- Market Dynamics: Japan’s pharma market features some large domestic companies (Takeda, Daiichi Sankyo, Astellas, Chugai which is part of Roche, etc.) as well as all the global multinationals present. Therapeutic wise, Japan has a big market for diabetes (owing to a high prevalence and early adoption of new drugs like GLP-1s and SGLT2 inhibitors), cardiovascular, and increasingly oncology (though some expensive immunotherapies have been introduced with restrictions to manage budget impact).

- Aging Population: Japan’s demographics (a quarter of population is 65+ and rising) mean demand for medications (for chronic illnesses, dementia, etc.) is high. However, the government’s fiscal pressures due to the aging population ironically force the cost cuts as they try to keep the system solvent.

In summary, Japan is a stable but low-growth market. It will likely slip from being #2 historically to #4 or lower by mid-2020s as China, and possibly if EU as a block considered, overshadow it. The focus in Japan has shifted to cost-effectiveness – in fact Japan recently introduced a sort of cost-effectiveness evaluation for some high-cost drugs to potentially adjust prices post-launch (somewhat akin to HTA, which historically Japan didn’t do).

Other Asia-Pacific Markets: India, South Korea, etc.

Beyond China and Japan, the rest of Asia-Pacific collectively is a sizable market:

-

India: India is a unique case – it’s one of the largest producers of pharmaceuticals (especially generics, supplying ~20% of the world’s generic drugs by volume) and has a large population of 1.4 billion. However, its domestic pharma market value is much smaller relative to its population because of lower spending per capita (many pay out-of-pocket, though government schemes are expanding). As of 2021, India’s pharma market was around $20–22 billion in sales ([36]), projected to grow to perhaps $30+ billion by 2025 on strong growth rates ~10% yearly. Key features: a huge generic industry (Indian companies like Sun Pharma, Cipla, Dr. Reddy’s dominate generics globally and domestically), increasing emphasis on branded generics – in India’s private market, docs often prescribe brand-name generics that compete in a branded generic marketplace. Healthcare infrastructure is improving and the government has launched some public insurance for poor populations (Ayushman Bharat), which could increase usage of medicines. The disease burden in India is shifting from infectious to chronic as well, boosting demand for drugs for diabetes (India has one of the highest numbers of diabetics), cardiovascular, etc. India’s drug pricing is typically very low; there is also a National List of Essential Medicines with price caps for key drugs. Therefore, while volume usage is huge, value remains lower. Internationally, India is critical because of its mass exports of generics and vaccines (the Serum Institute in India is the world’s largest vaccine maker, for example).

-

South Korea and Taiwan: These are high-income Asian markets with strong universal health systems. South Korea’s pharma market is ~$20 billion. Korea encourages local R&D too and some firms like Celltrion, SK Biopharma are emerging globally. Taiwan’s market is smaller (~$7–8 billion), but they have a robust generics usage and a single-payer that negotiates hard (Taiwan’s NHI is known to drive prices very low and even delist drugs if budget overshoots).

-

Australia: A developed market (~$14 billion) with a government Pharmaceutical Benefits Scheme that lists drugs and negotiates prices. Australia often references UK/Canada prices and is a mid-sized market with moderate growth.

-